5 Insights about Taxes: Easy Ideas for the Tax-Dreadful

Key Takeaways

Learning about taxes will move you away from feeling intimidated, and toward feeling intrigued.

A deduction is not the same as a credit.

Taxes are collected by multiple levels of government.

Certain types of accounts come with tax-related perks.

If you enter a higher tax bracket, only part of your income is taxed at that higher rate (not all of it).

We’re not supposed to pay our taxes once a year.

I started trying to understand personal finance for the first time when I was 39 years old. I devoured books, podcasts, and any material that shed light on the subject in plain language.

For the first time, I questioned my long-held assumption that I wasn’t the kind of person who concerned myself with personal finance.

For the first time, I began to feel the empowerment of knowing more than ever about how money works– the empowerment of seeing my options.

But one area of personal finance lagged behind the others, failing to earn my enthusiasm: taxes.

The truth: even if you loathe the topic of taxes, learning a tidbit here and there can be easy, and can come in handy.

The Tax Dread Epidemic

The world of taxes struck me as

Arbitrarily detailed

Painfully boring

Needlessly complicated

Changing too fast to learn

Can you relate?

I spent two weeks teaching middle school students a personal finance class I developed. I gave them an assignment: ask trusted adults a list of questions about money.

When asked what they wished they had learned earlier, only two of 80 adults mentioned taxes:

“I wish I had learned how to calculate taxes.” -A school counselor

“I wish I had learned about doing taxes.” -A teacher

If you…

dread the time of year you’re supposed to think about taxes

want to hire someone who understands it so you never have to

wonder how the average American is supposed to feel clear on the ever-changing details

… I get it!

If you feel tempted to dissociate when you hear tax-related advertisements and discussion, I can relate.

(I’ve heard of people who “love taxes.” If that’s you: I’m happy we have people like you!)

5 Easy Ideas About Taxes (Without the Complexity!)

Learning one little nugget at a time, over time, my knowledge has gradually expanded. My mind has slowly started to wrap itself around the deal with taxes.

Here are 5 insights to get you started.

1. A deduction is not the same as a credit.

A tax deduction reduces the amount of income that gets taxed. For example, a $1,000 deduction means if you earned $10,000, only $9,000 of it is taxed.

A tax credit reduces the amount of taxes you owe. For example, imagine you owe $3,000 in taxes. Then you apply a $1,000 tax credit, and you only owe $2,000.

2. Taxes are collected by multiple levels of government.

Nation: In the U.S., the IRS collects taxes on behalf of the federal government.

State: Different states have their own ways of collecting taxes. Some states, like Florida and Tennessee, don’t tax individuals’ income.

Town: Your city, township, or village has its own way of collecting taxes.

3. Certain types of accounts come with tax-related perks.

I like to picture accounts as containers for your money, like cookie jars.

Some account types are called “tax-advantaged” because they come with tax-related perks, or advantages. They apply advantages in different ways.

But the common thread is that you end up paying less in taxes with money (or investments) inside of them—compared to having that same money (or investments) in an account that’s not tax-advantaged.

A few examples:

HSA

529

Roth IRA

401(k)

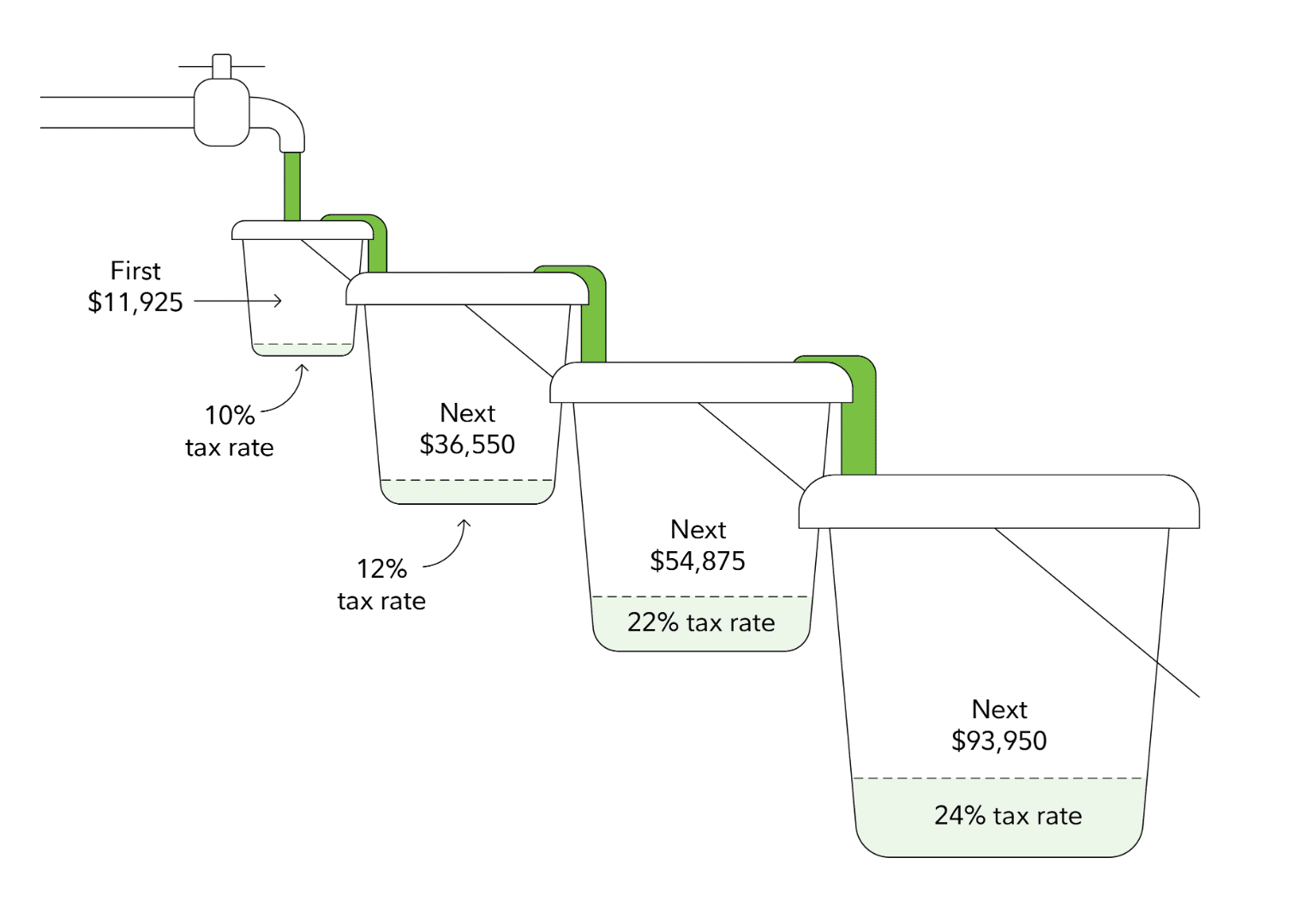

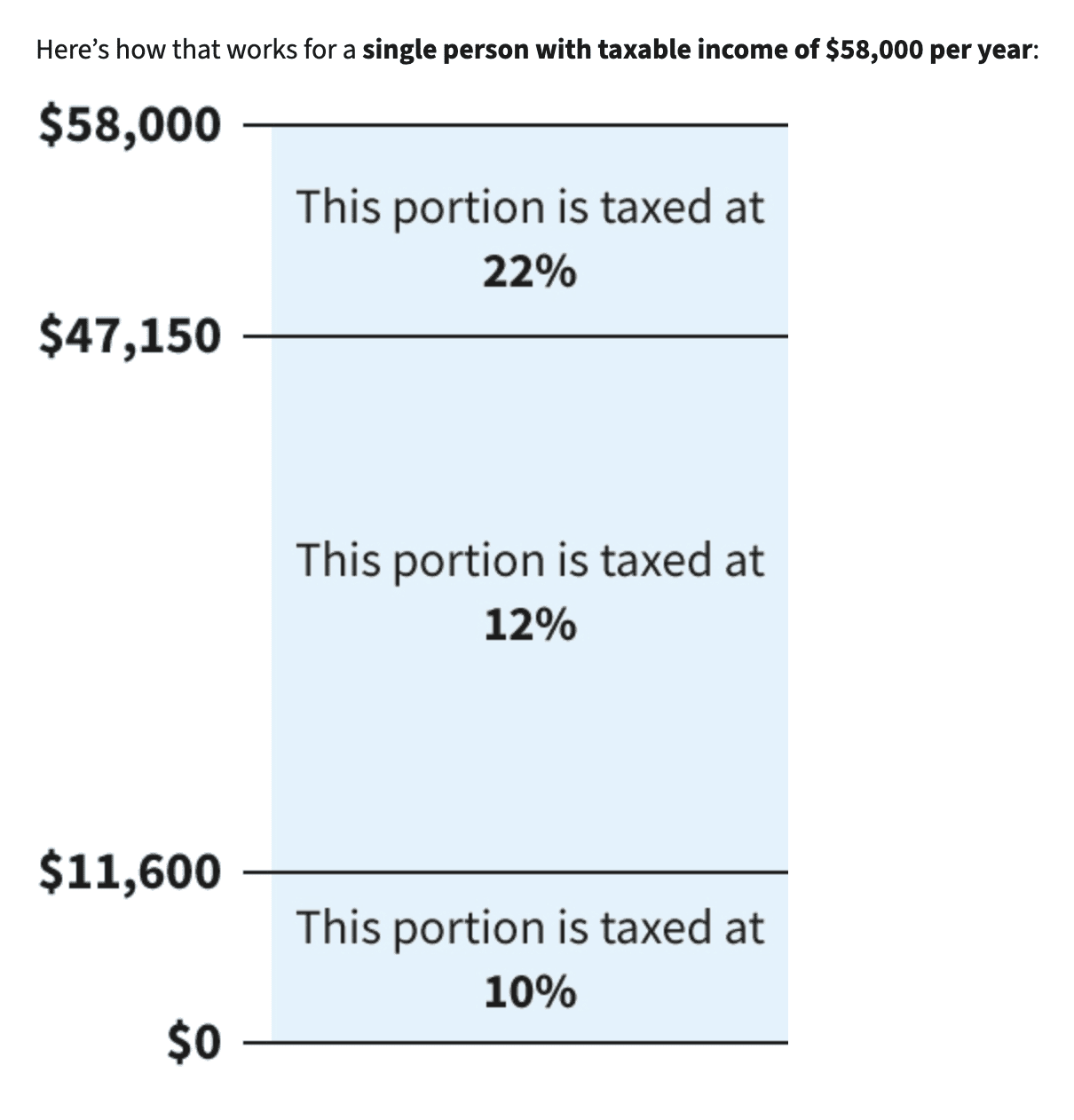

4. If you enter a higher tax bracket, only part of your income is taxed at that higher rate (not all of it).

Online comments reveal widespread confusion about taxes.

Pretend that earning over $100,000 bumps you into a 25% tax bracket (which is not the case, just an imaginary example).

And pretend earnings under $100,000 are taxed at 10% (which is not the case, just an imaginary example).

In that scenario, if you earn $104,000, you owe 10% of $100,000 plus 25% of $4,000.

So the first $100,000 is taxed at 10% and only the last $4,000 is taxed at 25%.

This is called a marginal tax rate.

Fidelity illustrates the concept with water filling up one bucket before it overflows to start filling the next.

The IRS depicts how only a portion of your income is taxed at your marginal tax rate.

The IRS depicts how marginal tax rates applied to a single filer in tax year 2024.

5. We’re not supposed to pay our taxes once a year.

The government wants taxes paid all throughout the year. It’s considered a pay-as-you-go system.

Your employer usually pulls out a portion of your income and does this for you throughout the year.

For other money you get, like self-employment or investment earnings, you’re supposed to send in quarterly estimated tax payments.

The Bottom Line

When it comes to taxes, keep in mind that no one person knows everything. Remember: it’s not all or nothing.

For those who already know this stuff: now you know that many adults don't. Try to keep that in mind as you interact with them.

For those who don’t know where to start: it’s ok if you’ll never be the type to geek out about taxes.

Just let yourself digest one nugget at a time. Then you’ll take a step away from feeling intimidated, and toward feeling intrigued.