The Billion-Dollar Mistake: Check Whether You’ve Made It, Too

Key Takeaways

Millions of people assume their investments are chugging along when they’re not.

Retirement means having the option not to work because investments earn the income that work used to.

Once or twice a year, make sure your accounts are still set up how you prefer.

If you have an investment account like a 401(k), IRA, HSA, or brokerage account—congratulations! You’ve taken an important step toward financial strength.

But beware: owning an account is not the same as contributing, and contributing is not the same as investing.

People assume that once the account is open, or once money is in the account, it’s automatically working for them. In reality, the account may be empty or idle, earning almost nothing.

That’s why it’s so important to take the next step: don’t just open an account; don’t just contribute; actually start investing!

The Common Mistake

Millions of people assume their investments are chugging along when they’re not. If you’re one of them, you’re not alone. I’ve worked with many clients who made this mistake—and I’ve made it myself!

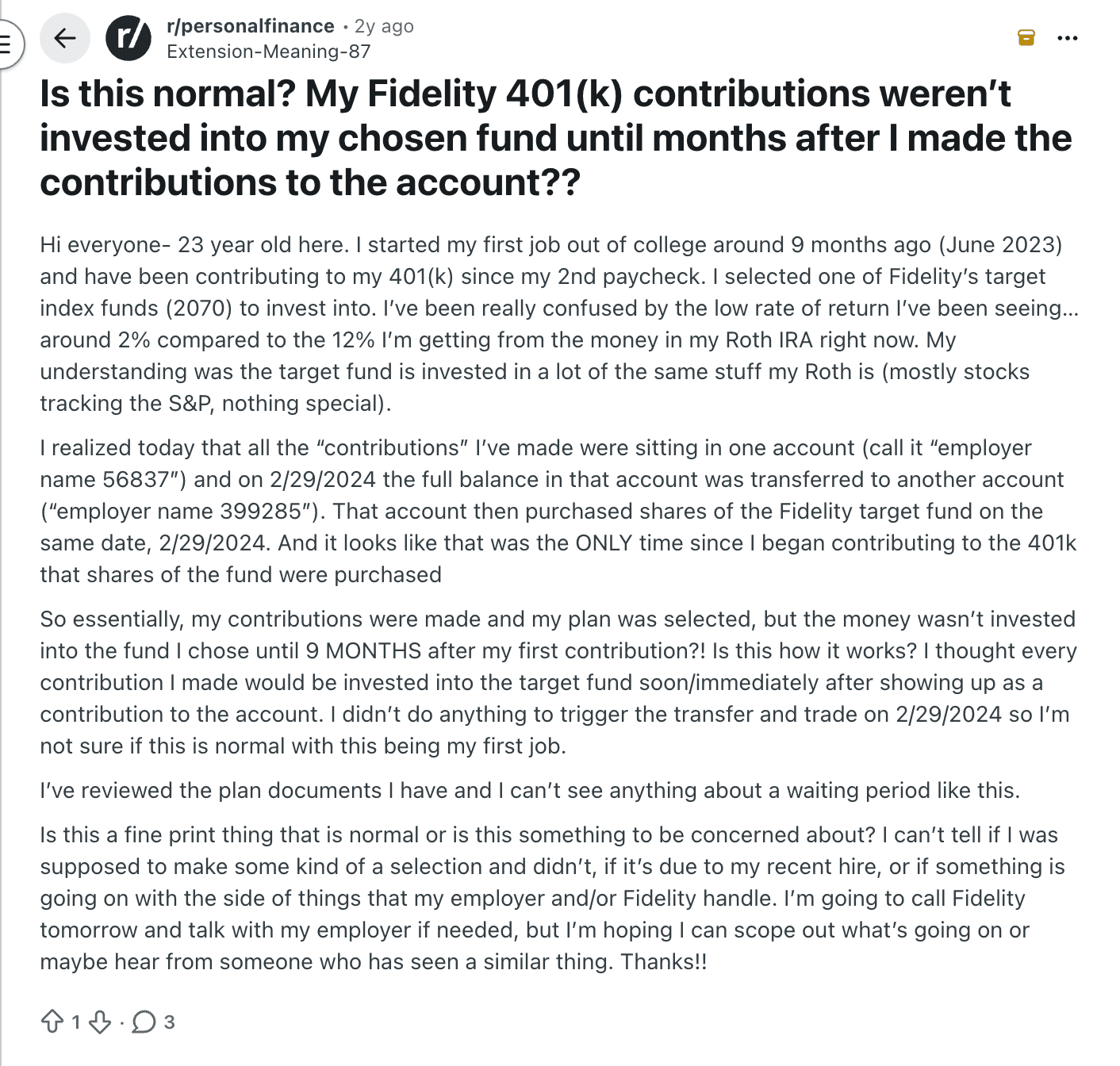

A Reddit poster discovered uninvested funds in a 401(k)

This happens in a variety of ways. For example:

You open an IRA because you heard it was smart. The account exists—the problem is you don’t contribute any money to it. So it’s worthless.

You set up automatic contributions to a Roth IRA. The money lands in your account like clockwork. But it lands in the “settlement fund,” the default landing pad for new contributions—growing insignificantly, waiting to be invested.

You part ways with an employer where you had a 403(b). You go through the process of rolling the account over into an IRA. When the balance arrives in your IRA, you assume your work is complete. The problem is part of the balance arrived as cash, not investments, keeping a portion of your future freedom on hold.

A Reddit poster accidentally left funds uninvested in a rollover account

What They Wish They Had Known

In my thirties, I wondered silently, “How do people retire? Maybe I’ll just hope that friends and family pitch in to help(?)”

I literally didn’t know how it worked. “It’ll probably work out somehow” felt more comfortable than the alternative.

At 39, my ignorance finally stung enough to motivate me to learn. Being honest with myself felt scary—but it was a crucial step toward hope and confidence!

I determined to learn as much as I could, and to help others do the same.

Now a financial counselor and educator, I spent two weeks teaching middle school students a personal finance class I developed. I had them ask a trusted adult, “What is a money lesson you wish you had learned earlier than you did?”

Among the responses:

“Investing.” - A mom

“Investing.” - Another mom

“Investing.” - A dad

“How to invest money.” - A mom

“Save in a Roth IRA sooner.” - A mom

“Don't just work for money. Make your money work for you.” - A mom

“I wish I had invested more when I was young.” - An uncle

“One money lesson I wish I had known earlier was investing. Honestly, if I had known how to put money in an index fund, we would be much better off.” - A parent

“It’s important to know your finances at a very early age. That way you’re prepared to invest.” - A parent

“Starting to save and invest early.” - A mom

“I wish I hadn’t taken money out of my retirement account when I was younger. If I could go back, I would put it back in.” - A mom

“Build up strong savings, and make investments early.” - A parent

If an older adult in your life has said to you, “Open a Roth IRA,” or “Contribute to your retirement account,” or any version of “Get started investing,” —they have your back! They’re trying to spare you regret.

Now I know the answer to my question, “How do people retire?”

For the most part, it’s investing. Retirement means having the option not to work because investments earn the income that work used to.

To honor the lessons others learned the hard way, and to expand our future options, we invest. This is why investing mistakes matter.

Real-Life Mistakes

I worked with a couple in their late 20’s who wanted to understand investing. In a financial coaching session, we discussed the basics of investing. They grew eager to get started. They opened their first Roth IRAs and set up automatic contributions.

In a later session, they peeked at their accounts. To their surprise, from the start 6 months prior, their contributions had never been invested. It was a quick fix—and a great save!

I worked with a young couple encouraged to open an IRA. They did exactly that, forgetting that funds still needed to be added. After two years, they noticed the oversight and began contributing.

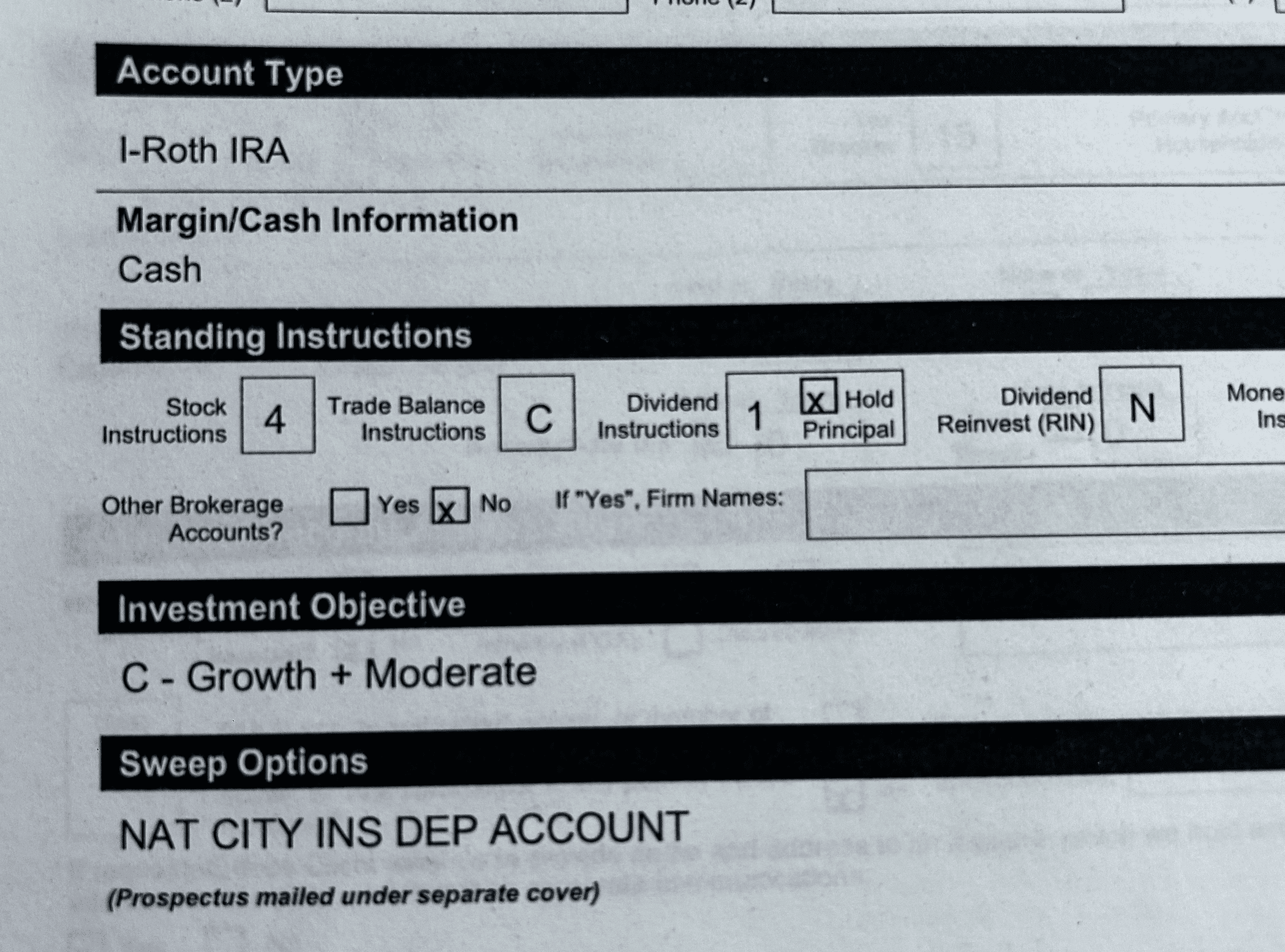

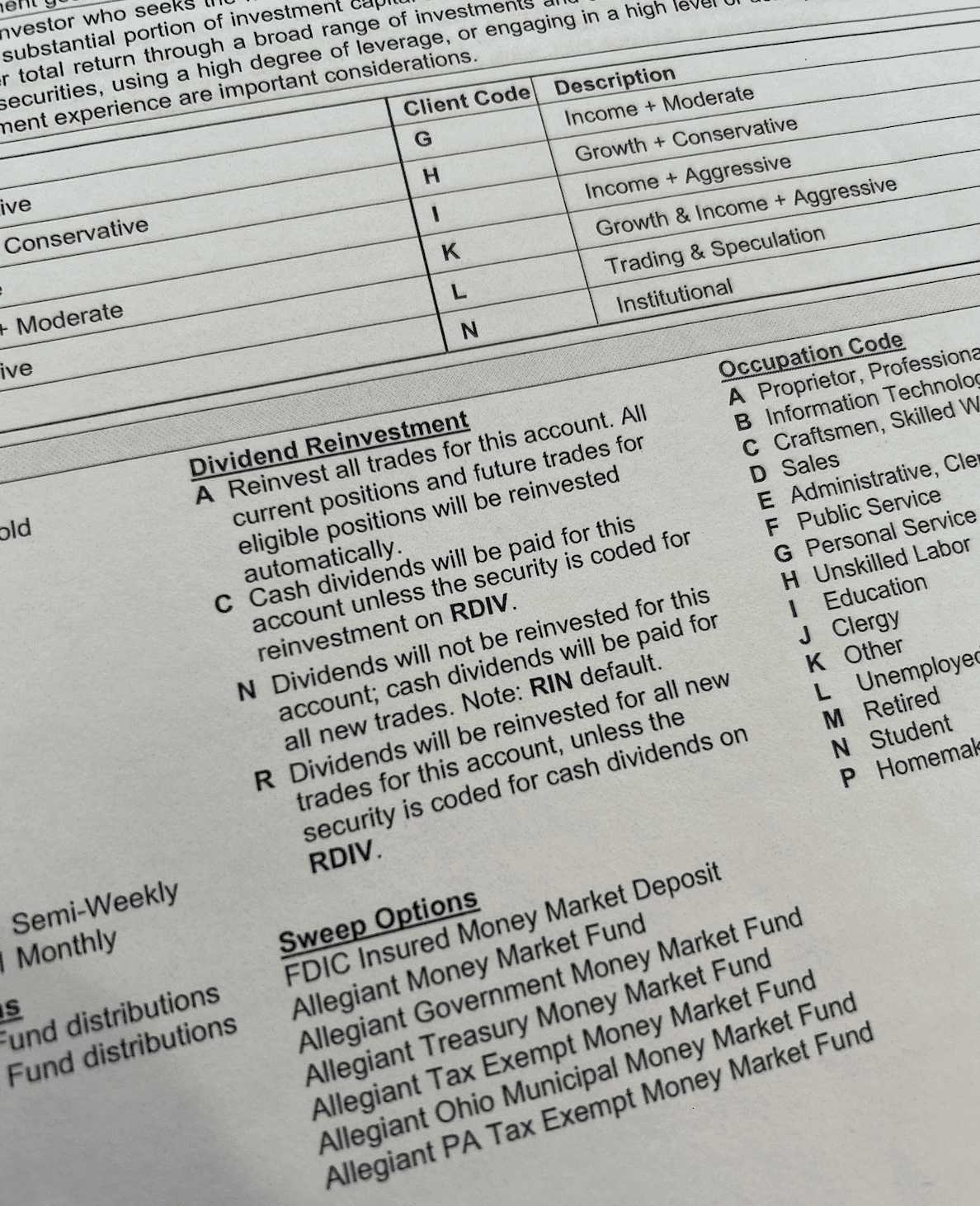

When I first opened a Roth IRA, I went to the bank to set everything up. Years later, understanding investing for the first time, I looked at the Roth IRA.

I was shocked to see half of it uninvested. I looked back at the original bank form: dividends weren’t being reinvested, for some unimaginable reason. This meant that a pile of uninvested cash had been building over the years.

The form that came home from the bank after opening a Roth IRA

The fine print says "N" means dividends will not be reinvested, which is also the default

Sometimes funds are rolled over from one account to another. Rolling over an account from a former employer is often a great idea, especially since people who don’t often lose sight of the account altogether. A 2025 study identified over 2 trillion dollars in forgotten retirement accounts.

But even the investors conscientious enough to do a rollover often make a tragic error: “Many investors unknowingly make a costly mistake when rolling their money from a 401(k) plan to an individual retirement account: leaving their money in cash.”

A study by Vanguard found that most rollover investors holding cash weren’t doing it on purpose; they just didn’t realize the money was uninvested.

If you still wonder whether this mistake is common—I just made it again this past fall.

In my Vanguard account, I canceled a monthly automatic investment, thinking I was pausing contributions. Turns out the contribution was a distinct automation, which I didn’t cancel. Those contributions continued, landed as cash, and, with the automatic investment turned off, stayed in cash— until I caught it 3 months later.

How to Actually Invest

How do you make sure your “investments” are actually invested?

Know Your Account

I like to imagine accounts as containers for your money, like cookie jars.

“Tax-advantaged” accounts come with tax-related perks. You ultimately pay less in taxes with tax-advantaged accounts, compared to having the same investments in an account that’s not tax-advantaged.

Each account comes with its own parameters, so get to know which types you have and which you want to get.

Some examples:

401(k), 403(b), 457(b) → through your employer

IRA, Roth IRA → not through your employer; you choose the brokerage and investments

HSA, 529 → tax-advantaged accounts for specific uses

“Taxable” brokerage account → easier to draw from, not tax-advantaged

Choose Investments

Instead of hand-picking a large assortment, many are happy with low-cost index funds or target-date funds, where one fund contains a large assortment bundled together.

Automate Contributions and Reinvestment

Fund the account by transferring money into it.

Set recurring transfers to add more money moving forward.

Find out how to get money invested immediately or as soon as possible after entering the account.

Check that dividends are reinvested.

Review Occasionally

Once or twice a year, make sure your accounts are still set up how you prefer.

The Bottom Line

Opening an investment account and adding money to it are great steps. These are actions of people who are strong with money. If you’re ready to take them, be sure to finish the process by investing the funds how you prefer.

If you started the process to make your money work for you, make sure your money isn’t sleeping on the job.

Take a look at what’s happening inside your investment accounts.

Then you can watch your investments—and future freedom—grow over time, in the direction you choose.