All You Need to Know About Investing in 5 Definitions

Have you ever started to learn about investing, only to get lost in a sea of jargon? The technical terms make investing feel overwhelming. No wonder so many people lack confidence.

Here’s the truth: you don’t need to know everything to be a successful investor. In fact, you only need to understand a handful of simple terms. If you tune out the intimidating language and grasp the key concepts, you’ll know enough to invest wisely.

What is an Emergency Fund?

Life throws curveballs. A flat tire, a surprise medical bill, or an unexpected job loss can shake your financial stability. Without a safety net, these events don’t just disrupt your routine— they can push you into debt, stress, and panic.

Your Financial Life Is Bigger Than Spending

If you see your spending more than other areas of your financial health, you are at risk.

For years, spending was the only aspect of my financial life that I saw.

Everything changed when I stopped seeing spending as the whole story.

Spending is the loudest part of your financial life. It demands your attention almost every day. Groceries. Gas. Birthday gifts. Shoes. Shampoo. The Costco run that magically turns into $353 every time.

There’s no opting out of spending. Adult life requires it.

Because spending is so visible, it’s easy to accidentally view your entire financial identity through the lens of spending alone.

You start to think personal finance is spending.

Your financial health is more expansive than checkout choices!

Just like physical health has multiple dimensions— strength, endurance, flexibility, sleep, nutrition, mobility, emotional health— your financial well-being also has many dimensions.

Spending is one of them— an important one, but just one.

Tradeoffs Made Simple: How to Say Yes Without Regret

Have you ever felt so excited to buy something you wanted, only to question yourself and feel guilty later?

Maybe it was a dinner out, a new phone, a piece of furniture, or a weekend trip. In the moment, you said yes wholeheartedly. Afterward, you wondered if that “yes” meant saying no to something more important.

Here’s the thing: every money decision involves a tradeoff, whether we like it or not.

But the tradeoffs don’t have to feel confusing or painful. Awareness of tradeoffs isn’t just about saying no. This mindset can help you say yes with confidence.

Pay Down Your Mortgage or Invest? The Tradeoff Worth Understanding

You’ve built stability. You’re covering your expenses. You’re contributing for retirement. You’ve even knocked out your high-interest debt.

When you make it to this point, you’re not just solving problems anymore. You think proactively.

You have a different kind of question:

What should you do with the extra money?

Do you send it toward your mortgage—chipping away at a decades-long obligation? Or do you invest it, putting your money to work for future growth?

This is one of those personal finance debates that never subsides. Like most debates that stick around this long, it persists because both sides make compelling points.

There’s Only One Right Way to Pay Off Debt (And Everyone Agrees)

Spend enough time in personal finance circles and you’ll start to think there are dozens of competing philosophies about how to pay off debt. One expert insists you should attack the smallest balance first. Another says that’s mathematically foolish; you should focus on the highest interest rate. A third tells you neither approach matters if you’re not simultaneously investing.

It sounds like disagreement. It sounds like conflict.

But amidst the noise, there’s an overlooked truth: they all agree.

There's only one good way to pay off non-mortgage debt. And it’s the same framework every credible personal finance educator teaches— whether they frame it differently or not.

Financial Strength Isn’t Built Overnight; Here’s How to Keep Growing

If you’ve ever wished for a quick fix to your money challenges, you’re not alone.

It’s captivating to imagine a quick route to financial success.

But here’s the truth: financial strength isn’t built overnight. Just like building physical strength or growing a tree, it takes time, consistency, and steady progress.

The great news is you don’t need a miracle to succeed, but you do need to keep growing, one step at a time.

5 Questions To Reveal What Matters Most in Your Financial Life

Most people manage their money on autopilot. They don’t have a game plan. They pay the bills, spend on whatever comes up, and save what’s left over—if anything.

The problem: Without intentionality, money slips away on things that don’t matter, leaving you perpetually stressed and unfulfilled.

The great news: You might not need more money to feel more in control. You might just need clarity.

When you see clearly how money connects to what matters to you, you see the control panel of your finances. You’re no longer in the dark, making mindless and misinformed decisions.

Instead of reacting, you start directing. Instead of chasing more, you can focus on what matters.

Here are 5 powerful questions to help you uncover what matters most in your financial life.

The Financial Advisor Scheme That Shouldn’t Be Legal (But Is)

I was recently on a group call for entrepreneurs learning about marketing.

During the call, another participant messaged me privately. She said we did similar work and asked if I’d schedule a call with her.

She mentioned she was pivoting into wealth management. I’m a financial coach, so that sounded like a natural connection.

We scheduled a call.

During our conversation, I learned that she was involved in a multi-level marketing (MLM) company selling life insurance products. She had hit rock bottom financially 6 months earlier, when a friend called, offering a wealth-building opportunity.

She didn’t explicitly pitch me on anything. She said she wanted to tell me more about the life insurance products and meet again the following week.

She mentioned she’s attending as many networking events as possible to find clients.

After the call, I found myself wondering:

How many other people from that group received the same message?

The Third and Final Behavior of Budgeting: Direct Your Money

When you think of improving your finances, many of you think: budgeting.

But strengthening your financial life is so much more than budgeting.

When you think of budgeting, many of you think, “I could never do that. Sounds like too much work!”

But we can break budgeting down into 3 distinct, doable habits.

Budgeting is not the most exciting aspect of growing money-strong. It’s also not the best starting point for everyone.

Some say they tried budgeting and it didn’t work. I have to wonder: was “budgeting” to blame, or was your concept of budgeting inadequate?

What someone calls “budgeting” differs completely from another’s understanding.

That’s why I like to give “budgeting” a thorough definition—specific enough to make an impact, while allowing flexibility and creativity in practice.

It’s a framework that’s useful for diverse, real-life humans— even those who never imagined they could get into budgeting!

In my Observe–Track–Direct framework, budgeting stems from three simple actions:

Observe – look at what your money is doing

Track – record your income and expenses

Direct – send your money where you want it to go

Observation creates awareness.

Tracking creates understanding.

Once those skills feel comfortable, you’re ready for the final phase: directing your money.

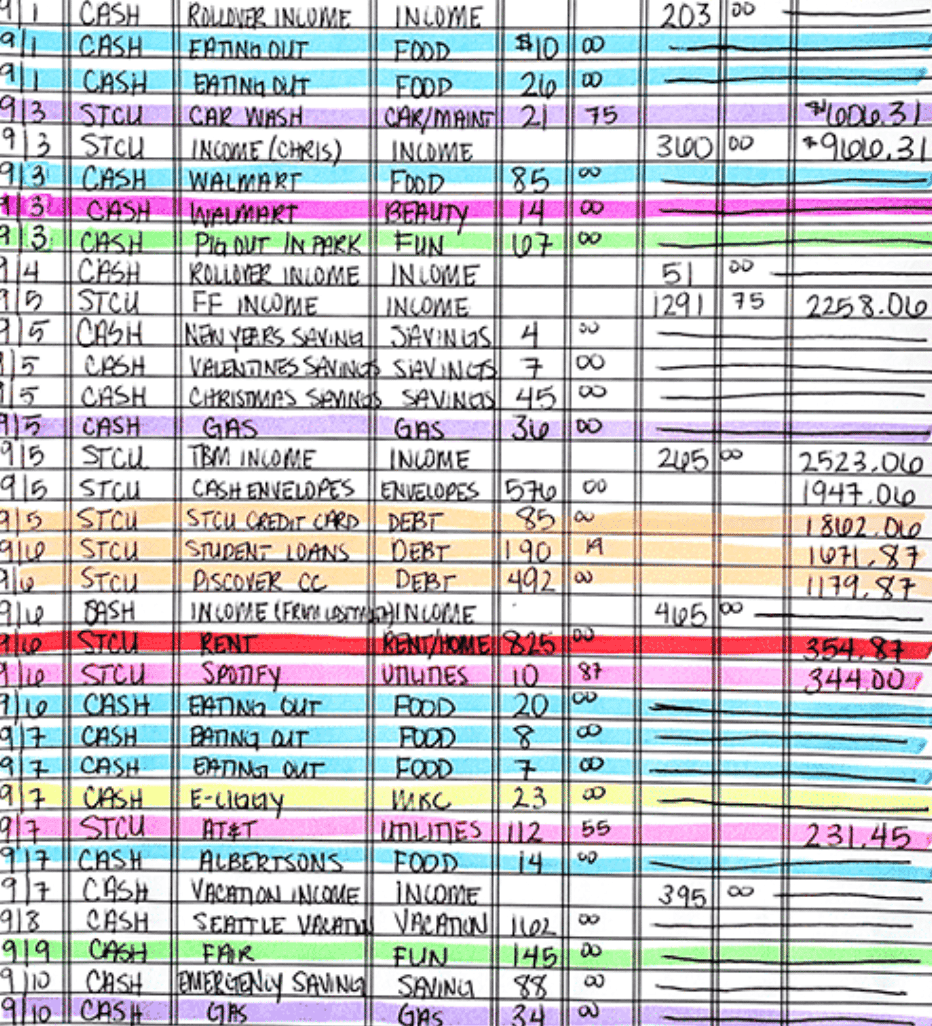

The Second Behavior of Budgeting: Track Your Money

Some people who say they keep a budget don't actually do what I consider real budgeting.

Sometimes they think they're budgeting because they keep a list or spreadsheet.

In my view, keeping a record of certain key numbers can be powerful, but only if joined with the other two essential habits of budgeting.

In my Observe–Track–Direct budgeting framework, budgeting stems from three simple behaviors:

Observe – look at what your money is doing

Track – record what you see

Direct – intentionally plan where your money will go

Once observing becomes a regular habit, you’re ready for the next step: tracking your money.

The First Behavior of Budgeting: Observe Your Money

When I hear people throw out the word “budget,” I often wonder if we’re talking past each other.

What exactly does budgeting mean?

If we don’t really know what we mean by “budgeting,” we can’t communicate about it, let alone do it.

I see budgeting as three behaviors layered on top of each other. That’s why I created the Observe-Track-Direct framework to define what I mean by “budgeting.”

Instead of trying to master budgeting all at once, this approach grows three skills one at a time:

Observe

Track

Direct

Together, these behaviors form a complete approach to budgeting.

Before you can control your money, you have to get comfortable simply looking at it.

That’s why this is the first component of budgeting: observe.

Budgeting Isn’t What You Think It Is

For many people, the word budget has a bad reputation.

Do you like the word?

Maybe you imagine someone hunched over a calculator, stressing over a spreadsheet. Maybe you picture strict rules, constant restraint, and saying “no” to things you enjoy.

For a lot of people, budgeting sounds like a lifestyle of restriction, deprivation, and limitation.

If that’s what budgeting really were, it would make perfect sense to avoid it.

Many budgeting approaches jump straight to control.

Real humans are the ones implementing these methods. So budgeting strategies must take human nature into consideration!

Why Lenders Want You Focused on Payments—Not Net Worth

When you’re looking to buy a car, or furniture, or open a credit card, you hear the pitch:

“It’s only $199 a month!”

Sounds manageable, right? That’s exactly the point.

Lenders don’t want you focused on the total cost of a purchase or how the debt affects your financial future. They want you focused on whether you can handle the payment—because that mindset keeps you borrowing longer and paying more in interest.

When you base spending decisions only on the cost of payments, you benefit the lender’s bottom line and neglect your own net worth.

How to Future-Proof Your Finances With Continuous Learning

If there’s one thing we know about the future, it’s this: things will change.

The job landscape shifts. Tax laws evolve. Technology creates new opportunities. What worked yesterday might not work tomorrow.

That’s why the smartest financial strategy doesn’t assume it’s already smart enough.

People who are strong with money stay curious.

If you want to safeguard your finances, stay curious as an ongoing learner.

Your Money Doesn’t Give You Value—You Give Your Money Value

Have you caught yourself thinking, “When I have more money, I’ll finally feel legitimate”?

Or, “I’m glad I’m not rich like those jerks”?

Does money make people better or worse?

In a world that often measures worth by income, image, and possessions, it can feel like your value as a person is tied to your financial status.

But here’s the truth: your money doesn’t give you value. You give your money value.

Money isn’t who you are. It’s a tool you use. And when you shift that perspective, everything about your relationship with money begins to change.

The Billion-Dollar Mistake: Check Whether You’ve Made It, Too

If you have an investment account like a 401(k), IRA, HSA, or brokerage account— congratulations! You’ve taken an important step toward financial strength.

But beware: owning an account is not the same as contributing, and contributing is not the same as investing.

People assume that once the account is open, or once money is in the account, it’s automatically working for them. In reality, the account may be empty or idle, earning almost nothing.

That’s why it’s so important to take the next step: don’t just open an account; don’t just contribute; actually start investing!

5 Insights about Taxes: Easy Ideas for the Tax-Dreadful

I started trying to understand personal finance for the first time when I was 39 years old. I devoured books, podcasts, and any material that shed light on the subject in plain language.

For the first time, I questioned my long-held assumption that I wasn’t the kind of person who concerned myself with personal finance.

For the first time, I began to feel the empowerment of knowing more than ever about how money works– the empowerment of seeing my options.

But one area of personal finance lagged behind the others, failing to earn my enthusiasm: taxes.

The truth: even if you loathe the topic of taxes, learning a tidbit here and there can be easy, and can come in handy.

Spending With Intention: How to Align Your Money With What Matters

Have you ever bought something and later wondered, “Why did I waste my money on that?”

Or maybe you’ve cut back so much that you feel guilty anytime you treat yourself.

Here’s the truth: money stress doesn’t come just from spending itself—it comes from spending without intention.

Seeing Your Money from Two Vantage Points: Why You Need Both and How They Differ

You want to get a better handle on your money, but you’re overwhelmed by all the moving parts:

Is an HSA the same as an FSA?

Should you check your credit score every day?

Are your student loans subsidized or unsubsidized?

Is the 0% credit card balance transfer actually free?

How can you keep everything straight? How do you know if you’re doing it right?