Net Worth vs. Credit Score: Which Number Actually Matters More?

Key Takeaways

Lenders use your credit score to predict whether you’ll repay borrowed money.

Knowing your net worth doesn’t benefit big companies, but helps you get a sense of your true financial picture.

Net worth tracks wealth. Credit score tracks borrowing power.

Aim for overall financial health, not just a credit score.

If you’ve ever applied for a credit card, car loan, or mortgage, you know the drill: lenders want your credit score. And if your score is high, you feel proud. If it’s low, you might feel embarrassed.

But here’s a secret: your credit score is not the best measure of your financial health.

Let’s explore the key differences between net worth and credit score, why lenders care more about one, and why you should care more about the other.

You'll notice marketers blur the line between your credit score and your "full financial potential."

Companies want your credit score to loom large in your mind.

Credit Score: What It Measures (and What It Doesn’t)

Personal finance educators like to say your credit score is like a financial GPA (i.e. your grade point average, like in school). I’ve heard some say your credit score is your report card.

But if it is, it’s primarily for the sake of lenders, less so for you.

Report cards and credit scores stir our feelings, but don't tell our story.

If you’ve ever felt like your credit score doesn’t tell the whole story of how you’re doing with money– you’re right! You know that lenders (or landlords) would get a better sense of your reliability if they got to know your personal situation.

But that would take a lot more effort, so they developed a formula to summarize your financial integrity with a number. The formula takes into account:

Payment history – Do you pay bills on time?

Credit utilization – How much of your available credit do you use?

Length of credit history – How long have you had accounts open?

New credit – How often do you apply for new accounts?

Credit mix – How many types of credit do you have (e.g. a mortgage is different from a credit card)?

Lenders want to predict whether you’ll repay borrowed money. The credit score is their attempt to do so.

But here’s the catch: your credit score says nothing about your savings, investments, income, or overall financial security.

You could have a stellar 800 credit score and still be living paycheck to paycheck, struggling with low income, or worried about overdrafting your checking account.

Sometimes a credit score will even decrease when you do something good with money! This is why it’s so important not to cater to your credit score.

I worked with a couple who was so excited about their aggressive plan to pay off student loans and finally be free from the burden. But I warned: once you pay off those loans, you may see your credit score take a temporary hit. That’s right– they may get dinged for their most admirable financial accomplishment to date!

The credit score gets more attention than it deserves, maybe thanks to the massive institutions who benefit from selling debt. It benefits them if you equate your credit score with your financial health.

Net Worth: A Bigger Picture

Meanwhile, there’s another number that doesn’t get the love it deserves.

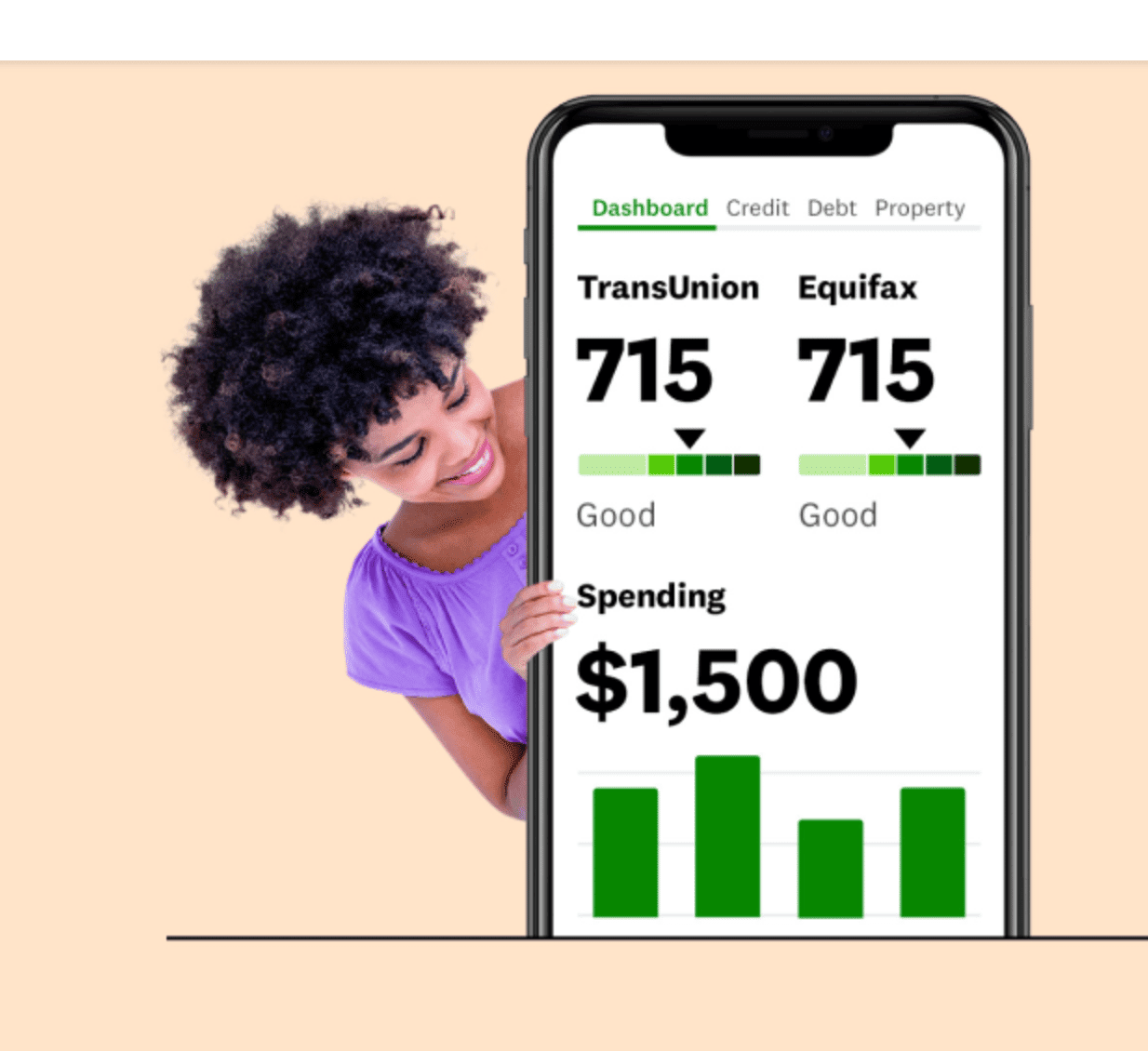

Did you know there’s not “a” credit score? There are hundreds of credit scores!

With your credit scores, there are many formulas, all of which are cryptic and complicated.

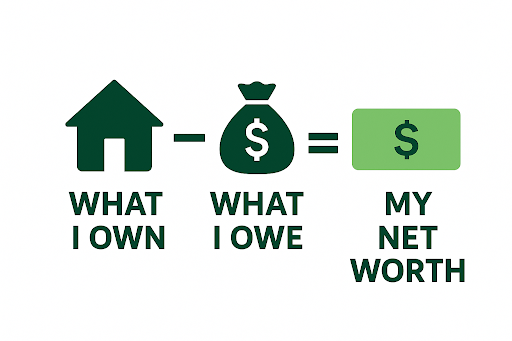

With net worth, the formula is simple:

Net worth = What you Own – What you Owe

Assets are things you own that have value: cash, retirement accounts, investments, property, and more.

Liabilities are what you owe: student loans, car payments, credit cards, mortgages, and other debts.

That’s why people say:

Assets – Liabilities = Net Worth

When you subtract liabilities from assets, you see your personal net worth—a number that doesn’t necessarily benefit big companies, but that helps you get a sense of your true financial picture.

Unlike your credit score, net worth doesn’t depend on how attractive you are to lenders. It’s a snapshot of how rich you are, monetarily, at a moment in time. If you track it regularly over time, it’s a number that tells you whether you’re building wealth or staying stuck.

Think about it. Lenders profit when we consumers borrow money–at our expense. They get excited when we spend more money than we actually have. That’s where their priorities lie. But should we share priorities?

Today I got (yet another) email from Chase entitled, “Great news, Lesley! You’re preapproved for up to $75,000 in auto financing.” How do I break it to them that I’m not as overjoyed as they are?

I understand it’s an opportunity to own a vehicle and have transportation, which certainly has value.

But I also understand that the $75,000 they’re so excited about isn’t just money into my life—it’s money out of my life.

In my net worth calculation, the $75,000 would count as the opposite of money—negative money. It would become “what I owe” and detract from my net worth.

At the end of the day, net worth tracks wealth. Credit score tracks borrowing power.

Your life is building purpose and value over time, and you want wealth to undergird that, not just borrowing power.

The Trap of Focusing Only on Credit

It’s easy to see why people obsess over credit scores. Credit card companies, auto lenders, and mortgage brokers reinforce the idea that your score is everything.

I remember buying a used car at the dealer in December of 2023. I wanted to pay cash. They said I could run to the bank or write a check, but in the latter case, they would have to run a credit check.

I didn’t want to run another errand, so I said, “fine” to the credit check. Up to this point, my understanding was that the credit scoring system went up to 850. So when they announced my credit score was 860-something, I did a double take.

“What? I thought it only went up to 850.”

“No, this one goes higher.”

For a fleeting moment, it felt kind of cool to have an off-the-charts score. But it’s important to me not to get emotionally tied to my credit score. It’s a moving target. It’s one of hundreds of credit scores. It’s overly complex.

This is the car I bought.

The car dealer was looking at my score to answer the question: “Will this customer’s check bounce?” Of course, I didn’t need a number to know that my check was good. And I didn’t need to feel like a rockstar because I don’t write checks that bounce.

Resist the temptation to take your credit score too personally. Pride, shame, or worry about the score itself could be a sign that you’re placing too much focus on it.

Focusing only on credit can lead to financial traps:

The minimum payment mindset – “As long as I can afford the monthly payment, I’m fine.” In reality, that thinking often leads to more debt and less wealth.

Borrowing for status – High credit can make it tempting to take on more debt for things that depreciate (cars, clothes, vacations).

Mistaking borrowing power for financial security – Just because a lender approves you for a loan doesn’t mean you can afford it comfortably.

Lenders profit when you focus on your credit score. You profit when you focus on your net worth.

Balancing Both Metrics

This doesn’t mean your credit score is irrelevant—it still matters for practical reasons like renting an apartment or qualifying for a mortgage.

But it’s important to understand the difference:

Credit Score = Lender’s tool (shows how well you handle debt).

Net Worth = Your tool (shows how close you are to financial independence).

Here’s a reality check:

You can have a 780 credit score and a negative net worth if you’re buried in student loans or credit card debt.

You can have a modest 650 credit score and a growing positive net worth if you’ve built savings, investments, and paid down debt.

The key is to treat your credit score as a supporting character, not the star of the show.

Aim for overall financial health, not just a number.

To check your financial health, make sure you take the Money Strength Assessment.

Pay more attention to net worth and less to credit score. You’ll find that a good credit score can be a side effect of financial health, even when it’s not the focus.

How to Shift Your Focus

If you’ve been obsessing over your credit score, don’t worry. Shifting your focus to net worth is straightforward:

Calculate your current net worth.

List what you own (assets): cash, savings, retirement accounts, investments, property.

List what you owe (liabilities): all debt balances, from credit card balances to student loans to mortgages. Remember you are looking for the running total that you owe altogether, not monthly repayment amounts.

Subtract liabilities from assets.

Track your progress regularly.

Update your net worth quarterly or twice a year.

Don’t obsess over small fluctuations—focus on long-term trends.

Take action to grow it.

Increase assets: save consistently, invest wisely, build income streams.

Decrease liabilities: pay down debt strategically, avoid unnecessary borrowing.

Adopt the net worth mindset.

Stop measuring success by how much you can borrow.

Start measuring success by how much you keep.

The Bottom Line

Your credit score matters—especially to lenders. It determines how easily you can borrow money.

Your net worth matters even more—to you—because it measures your wealth, which undergirds the purpose and value your life aims to build.

So if you’re focused on your credit score, show some love to your net worth, a number that bolsters your journey to grow money-strong.