The Secret to Stress-Free Saving: Work with Your Brain, Not Against It

Key Takeaways

Saving doesn’t have to feel like a battle of discipline.

You can “trick” your brain into painless, even fun, saving.

When you work with your brain instead of against it, saving becomes easier.

When you think of saving money, what comes to mind?

For many people, it’s sacrifice, stress, or restriction. Saving feels like giving something up today— fun, convenience, enjoyment, opportunity— for a theoretical payoff far in the future.

No wonder it’s hard to stick with it.

But here’s the good news: saving doesn’t have to feel like a battle of discipline. Don’t just tell yourself, “I really need to try harder not to spend so much next month.”

Trick your brain into painless, even fun, saving.

You can make it easier by working with your brain instead of against it.

Why Saving Feels Hard

If you’ve ever struggled to save consistently, you’re not alone. It’s not because you’re bad with money— it’s because you’re human.

Our brains are wired for instant gratification. We’d rather have something now than wait, even if what we get later is better.

Psychologists call this “present bias,” our natural tendency to value rewards we get today more heavily than future positive or negative consequences, even if the future consequences are bigger.

With present bias at work, when you add money to your savings account, your brain registers a loss.

Rather than feeling a win, it’s as if you took a hit, psychologically. You don’t get to eat out, shop, or upgrade something. The number in your checking account goes down.

Perhaps you know the benefits of saving, intellectually, such as future peace of mind, future security. But the benefits feel foggy and abstract, not compelling.

In this situation, the healthy financial behavior that brings the greatest rewards— bigger, better results tomorrow— feels like a punishment.

This mismatch makes saving feel onerous.

The cliché advice, “just spend less,” only adds guilt to the mix. Why keep pushing yourself to make choices that feel bad?

When you consider how your brain works, you can design routines that make saving feel easy, natural, even exciting.

How to Trick Your Brain Into Saving

Here are five brain-friendly tricks that make saving feel better:

1. Pay Yourself First

Instead of saving “whatever’s left,” prioritize savings like you would a non-negotiable bill. You don’t start every month wondering how much of your phone bill you’ll pay; you just pay it like clockwork. With this trick, the money you want to save comes out first, before you spend. Psychologically, this shifts saving from optional to essential.

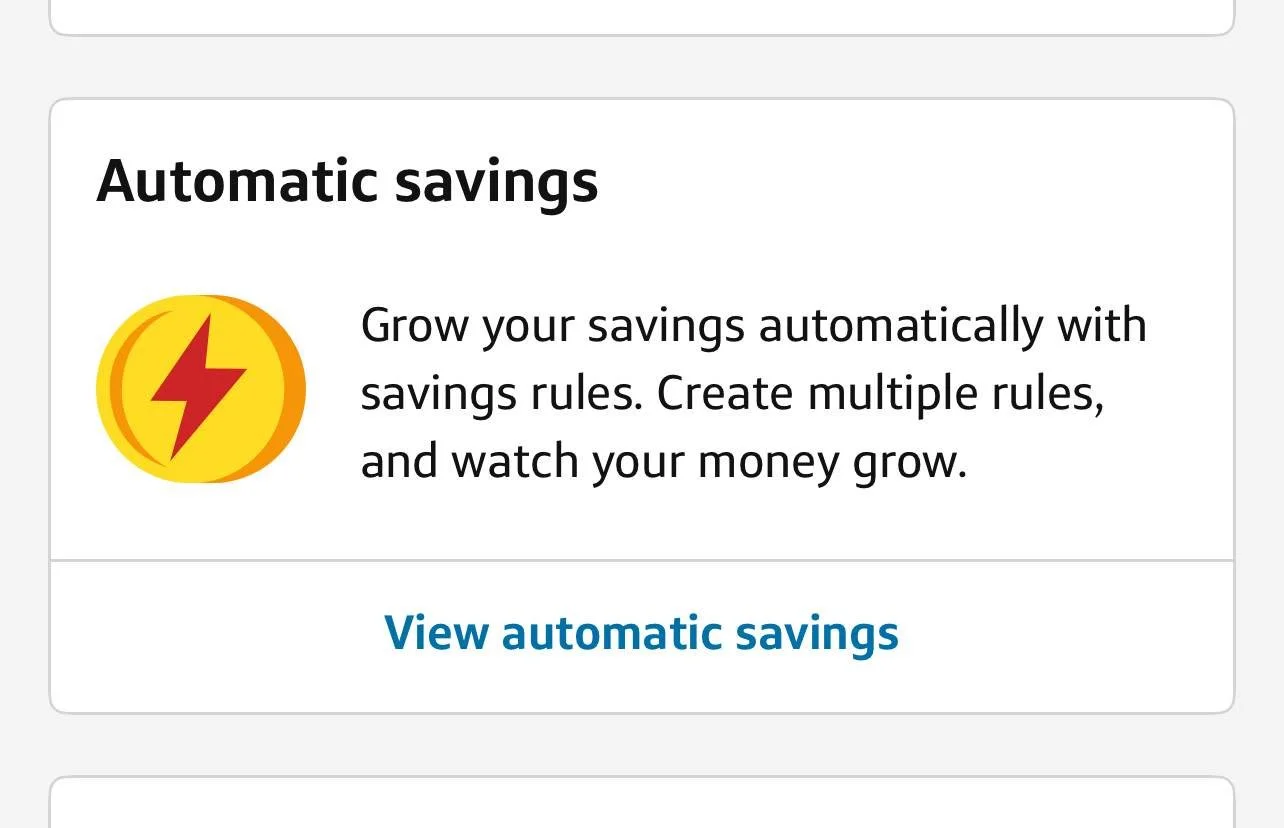

2. Use Automatic Transfers

Automation removes choice, chance, and resistance. If your bank or employer can send part of your paycheck directly into savings, you’ll soon learn not to miss it. No decision required, no stress, no effort.

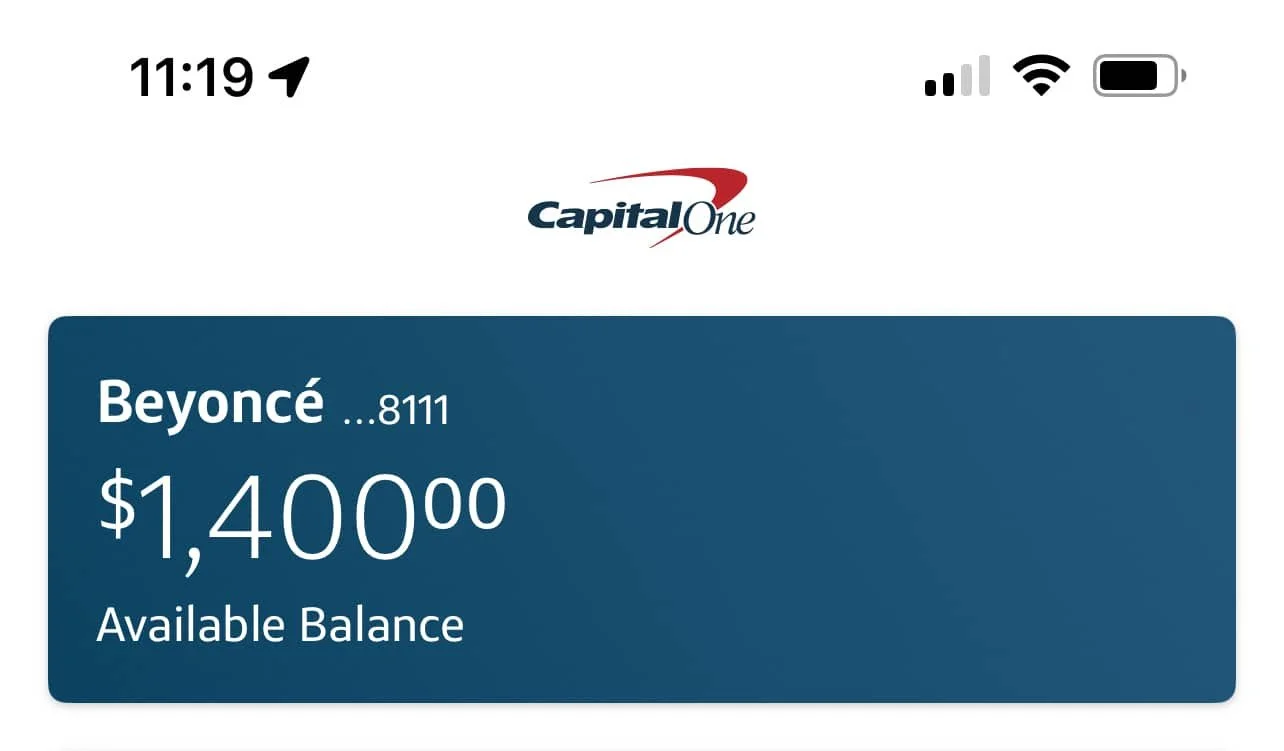

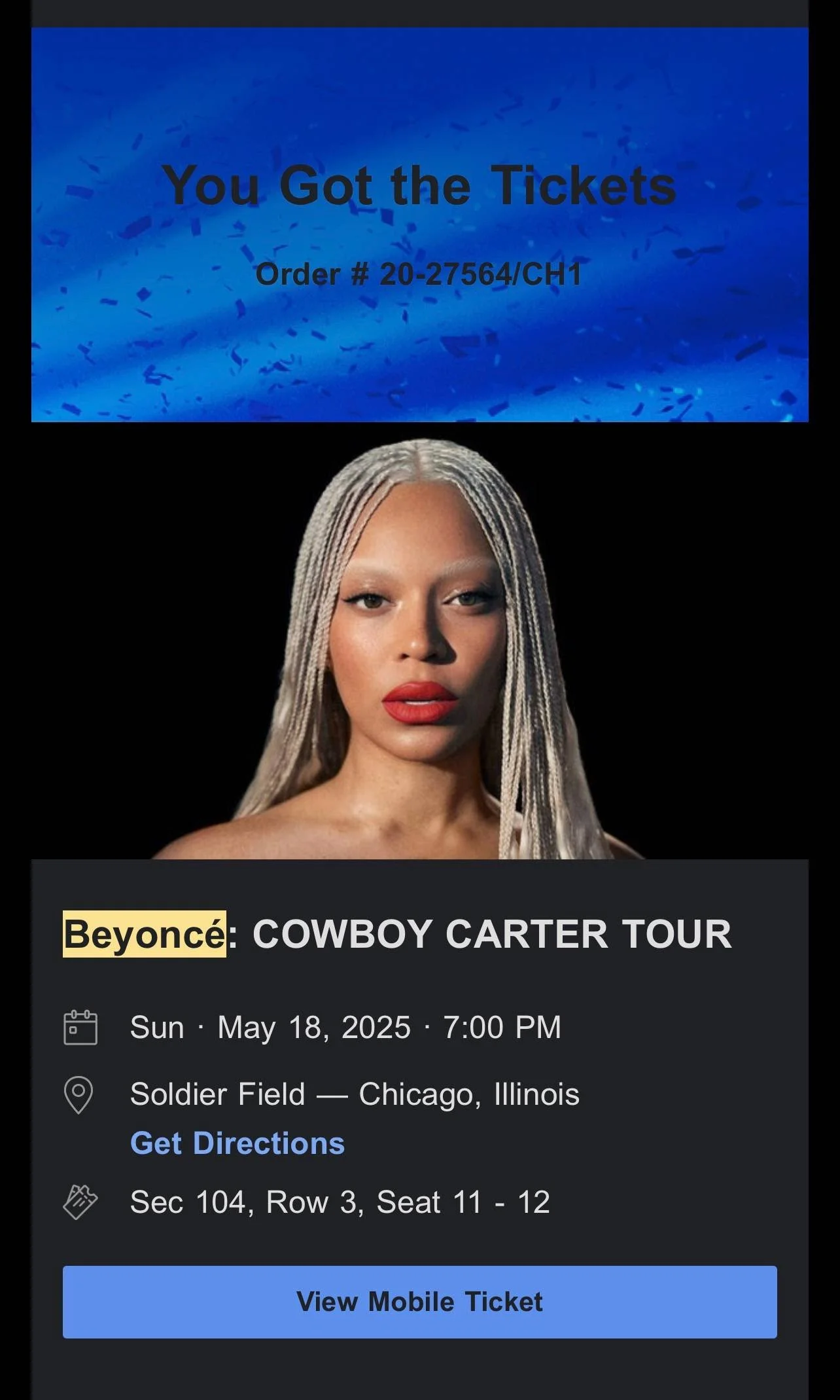

3. Name Your Accounts

Here’s a powerful hack: give your savings accounts specific names. Vivid titles like “New Zealand 2028,” “New Lexus Fund,” “Dream Wedding,” and “Peace of Mind” feel motivating. Building your savings isn't just fiddling with numbers; it’s intentionally placing powerful life experiences in your path.

4. Make It Fun

Gamify the process. Create a 30-day savings challenge, post a visual progress tracker on your bathroom mirror, or celebrate specific milestones. Bridge the gap between your experience today and your long-term satisfaction by making savings goals fun. You keep the momentum with dopamine hits as you reach benchmarks. Saving can feel like winning today, not just tomorrow.

5. Out of Sight, Out of Mind

Keep savings separate from checking, whether visually, mentally, or however you need. This money should be distinguished from your main cash account, not sloshing around with your normal spending money. Get to know yourself and how out-of-reach you want your savings accounts. Some like to make savings hard to access, while others find it gratifying to see their balance growing on a regular basis.

Why These Tricks Work

These tricks succeed because they factor in how your brain naturally operates:

You rely on habits every day. It’s great when you can accomplish essential tasks, like breathing, without a second thought. Like a talented musician, your actions are no less important when they use muscle memory. Automatic transfers nurture your financial health with effortless routines.

Your sense of identity matters. There’s a gap between how you handle your money and who you ultimately want to be. Naming your savings accounts connects your saving behaviors to your authentic self (e.g. the traveler, the homeowner, the loving parent, etc.).

You honor your psychological needs. You deserve to feel like you’re making gratifying choices today, in real life, not just doing the right thing on paper.

Instead of framing saving as loss, these strategies reframe savings as gain. And that makes all the difference.

Real-Life Impact

I worked with a couple who had a hard time finding the motivation to put money in savings.

With $52,000 in non-mortgage debt and $950 in a savings account (and a child, two dogs, a house, and three vehicles), their savings would have covered a Monday, Tuesday, Wednesday, Thursday, and half of a Friday (4.5 days worth of their family’s monthly expenses) before falling to zero.

They said they knew they “should” save but felt drained and unmotivated at the thought of doing so.

“What if we work hard and sacrifice for 5 months, stash away $2,000 every month, build our savings account up to $10,000, then encounter an emergency that costs us $10,000? All of our self-denial will have been in vain. How are we supposed to feel motivated to save, knowing it could all get undone anyway?”

They said it would feel better to use debt to finance a $10,000 emergency, rather than give up $10,000 of cash they had saved by going without for 5 months.

In other words, they felt the pain of loss when they saved, but not when they deepened their debt.

What would you say to this couple? Do you see present bias at work?

The credit card industry runs on the fuel of your present bias.

It’s expert at making future harm feel painless today.

Like many of us, this couple had disconnected from the reality of how much interest they were paying on their debt.

I call it throwing money into the wind, because it’s going toward nothing meaningful for your family. That’s what I consider draining.

Like most of us, they hadn’t kept a close eye on their income and expenses or tabulated the total amount they were paying toward non-mortgage interest every month.

So of course it felt painless.

In our time together, we finally looked.

They were throwing $2,634 every month into the wind.

“What could your family do with $2,634 each month, besides throwing it to the wind?”

In a moment, their feelings changed. Suddenly, they associated their debt with pain and loss.

In our time together, we reframed the prospect of spending saved money.

Now when they set aside money in savings, and occasionally spend the money they’ve saved, they don’t feel weakened. Instead, it’s a power move. They can say “No way” to throwing their family’s money into the wind.

The Bottom Line

Saving isn’t just about numbers. It’s about psychology.

You don’t have to pressure yourself to save, then feel terrible as you try! When you work with your brain instead of against it, saving becomes easier.

Learn to make saving feel rewarding both today and tomorrow.

Give your brain what it wants while giving your future what it needs.