There’s Only One Right Way to Pay Off Debt (And Everyone Agrees)

Key Takeaways

It feels like the internet is constantly arguing about the “right” way to pay off debt because personal finance gurus, want to stand out.

The one right way to payoff non-mortgage debt:

Make a list of your debts.

Rank them in order.

Target one at a time.

Roll your progress forward.

Keep going until you’re done!

The difference between financial progress and stagnation isn’t choosing the optimal strategy but taking action.

Spend enough time in personal finance circles and you’ll start to think there are dozens of competing philosophies about how to pay off debt. One expert insists you should attack the smallest balance first. Another says that’s mathematically foolish; you should focus on the highest interest rate. A third tells you neither approach matters if you’re not simultaneously investing.

It sounds like disagreement. It sounds like conflict.

But amidst the noise, there’s an overlooked truth: they all agree.

There's only one good way to pay off non-mortgage debt. And it’s the same framework every credible personal finance educator teaches— whether they frame it differently or not.

The One Right Way to Pay off Debt

Start by listing every debt you have. Include the balance, minimum payment, interest rate, and projected payoff date. Get it all out of your head and onto paper (or a spreadsheet).

Next, arrange that list in the order that motivates you most. Not the order someone else tells you is “correct”— the order that makes you want to act.

Then, prioritize overpaying the debt at the top of your list. Put every extra dollar you can toward it while continuing to make minimum payments on the rest.

Once that debt is gone, redirect that same money and energy to the next one.

Repeat the process until all your non-mortgage debt is paid off.

That’s it. That’s the system.

Everything else is just the icing of personal preference layered on top of this cake.

Why it Doesn’t Feel that Simple

If the core approach is so widely agreed upon, why does it feel like the internet is constantly arguing about it?

Because personal finance gurus, like anyone with an audience, want to stand out.

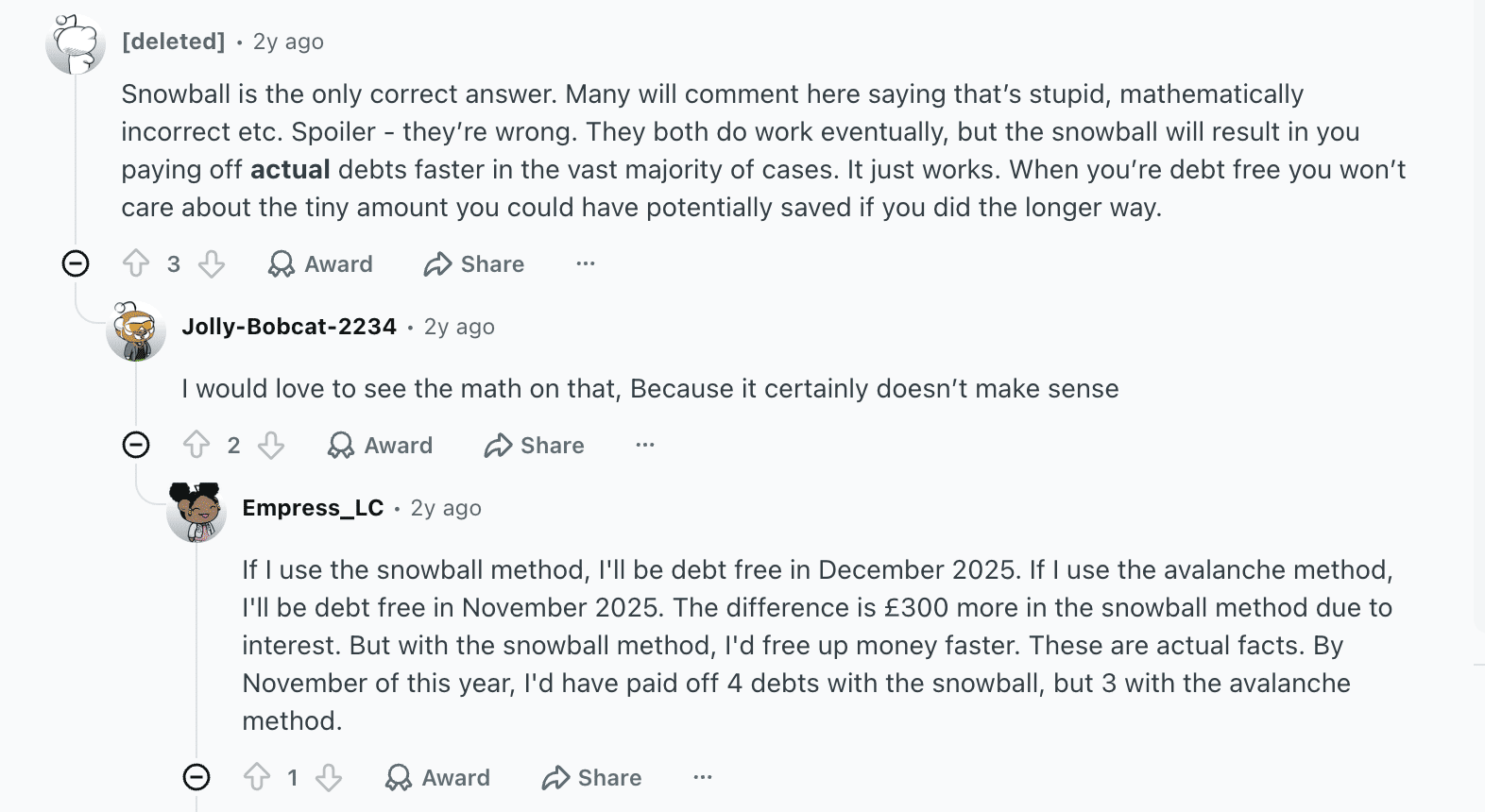

Redditors trying to one-up each other

Clear, polarizing statements attract attention far better than nuanced ones. “Everyone else is wrong” is a much more clickable message than “There are tradeoffs worth considering.”

So you’ll often hear takes that sound like this: “The others say this, but it’s actually that.”

When you hear that tone, it’s worth taking note.

Not because the person is necessarily wrong, but because they might be trying to differentiate themselves more than they’re trying to help you.

Real-Life Impact

I’m sensitive to the disservice money educators do, bombarding audiences with jargon and cyclical debates.

I remember moments in my 20’s and 30’s that could have marked my entry to learning more than ever about money, but the door stayed closed.

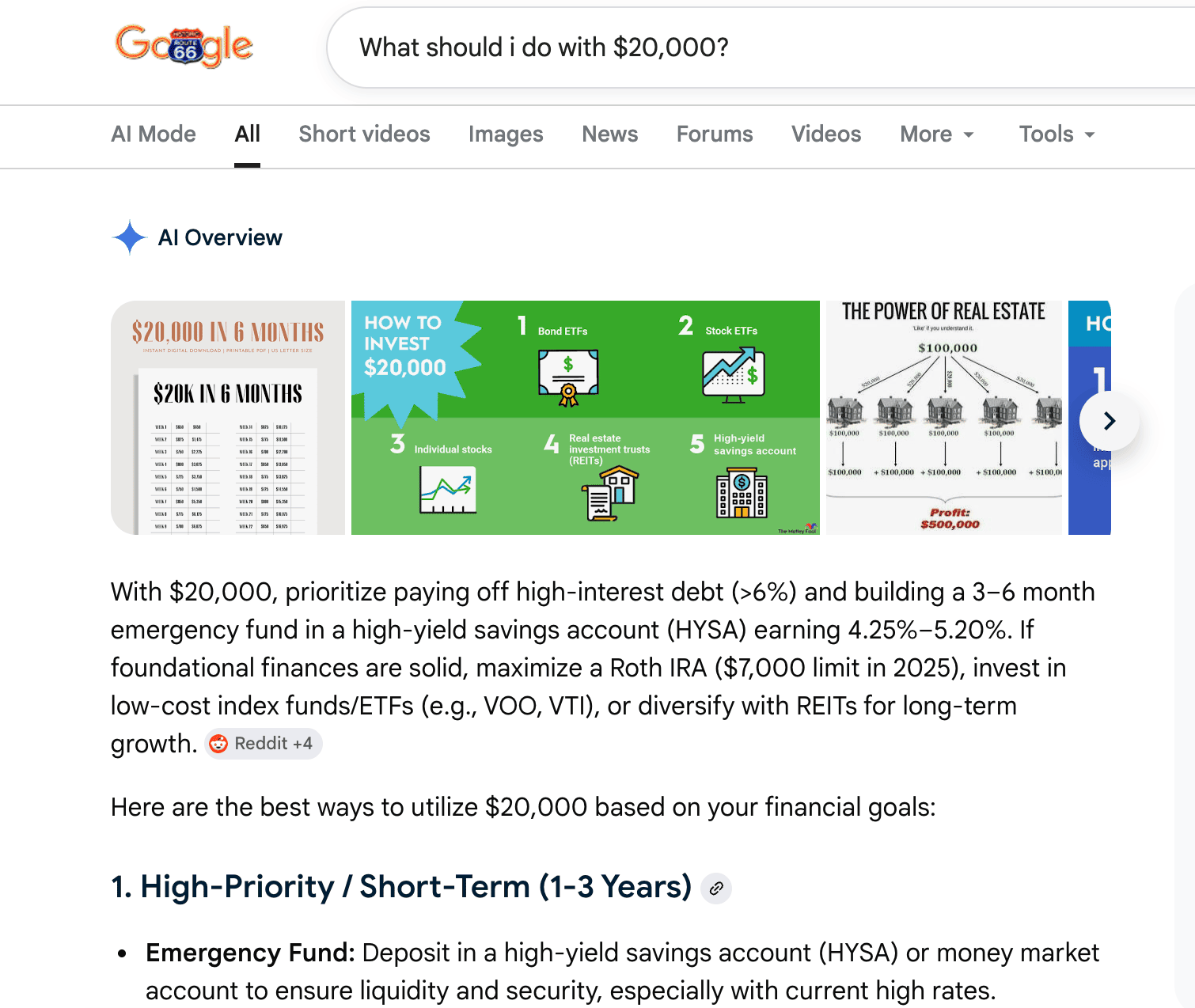

After cashing out a few permanent life insurance policies that had been given to my husband and me, I Googled “What should I do with $20,000?”

The search results (before AI search results!) were like Greek to me.

I'm not sure today's AI overview would have served me much better. When I saw this kind of jargon, I thought it meant I could never break in to this world of personal finance understanding.

I found blogs with ranked lists of financial products to purchase with my $20,000 (in hindsight, they were paid sponsorships). I didn’t understand what any of the options even meant, or why I would choose them.

So I settled for a few more years of confusion, saying, "I'm not a money person."

I worked with clients— astute, educated, driven to learn— who fell victim to the noise. This couple understood the dangers of consumer debt. They normally avoided it.

Unexpected life events landed them with a few credit card balances they couldn’t pay off immediately. They knew they wanted these gone, and they knew they should pay more than the minimum.

Despite reading regularly about personal finance online, they took a debt payoff approach that no one recommends, but many follow: Whenever they noticed cash in their checking account or otherwise felt inspired, they logged into a credit card account and plopped an extra payment on the balance.

They did this for each of 3 credit card balances, multiple times per month.

By not targeting one debt at a time, they inadvertently prolonged their time with all of them!

Fortunately, our conversation in financial coaching sessions quickly brought this to light.

They saw the value of the only right way to pay off debt, and they instantly put the plan to work. They paid off all 3 of their credit cards in just 4 months— and lifted a weight off their family’s shoulders!

When I see the life-changing power of clarity, I resent all the noise, and I fight that much harder to cut through it.

Signs of an Unproductive Debate

Once you start looking for it, you’ll notice patterns:

A personal finance guru disparages a financial choice that thousands of financially strong people have made without regret

Each side oversimplifies or mischaracterizes the other to make their argument look better

The conversation drifts toward absolutes: always, never, right, wrong

These are your cues. That’s when it’s time to resist the pull toward an all-or-nothing mindset.

The Debates that Never Seem to Die

You’ve probably seen some version of these:

Should you prioritize a high-interest debt or a low-balance debt first?

Should you pay extra toward your mortgage or invest instead?

Should you accelerate debt payoff or build a larger emergency fund?

Should you “budget,” or follow a system that avoids using that word entirely?

Each of these debates gets framed as if there’s a single correct answer.

There isn’t.

There are tradeoffs.

And there are people thriving on both sides of each decision.

The problem isn’t that these conversations exist; it’s when someone presents their preferred approach as the answer.

Where Rules of Thumb Still Matter

To be clear, there are areas in personal finance where rules of thumb are useful. Simple guidance helps people get started, especially when they feel overwhelmed. I myself spout plenty of unequivocal, unapologetic principals (see article title above).

But even then, those rules should be understood as starting points, not universal laws.

The goal isn’t to memorize someone else’s system. It’s to understand your options well enough to choose intentionally.

What Actually Moves the Needle

For most people, the difference between financial progress and stagnation isn’t choosing the optimal strategy.

It’s taking action.

You can waste hours debating the debt avalanche versus snowball. Or you can pick one, start paying extra, build momentum, and stride as fast as possible toward debt-freedom!

Implementation beats optimization!

That doesn’t mean the nuances don’t matter. They do. Exploring both sides of a decision helps you see the tradeoffs more clearly. It deepens your understanding and gives you confidence in your path.

Seeing the validity in both sides enriches you more than committing blindly to one.

But there’s a point where learning stops being productive and starts becoming a distraction.

Don’t Miss the Forest for the Trees

Many personal finance educators possess genuinely life-changing knowledge—knowledge that too many people never encounter.

That’s why it’s frustrating when so much of the conversation gets spent pitting two valid approaches against each other.

Because the regular person outside of that universe— the one just trying to get their finances in order— doesn’t need another debate.

They need a starting point.

So here it is again (stripped of branding and noise), the one right way to payoff non-mortgage debt:

Make a list of your debts.

Rank them in order.

Target one at a time.

Roll your progress forward.

Keep going until you’re done!

The Bottom Line

Don’t let the endless rabbit hole of financial debates distract you from doing the work itself. Choosing a path and following through will always beat waiting around for the perfect one.

And to turn my own words back on myself: maybe those black-and-white takes serve a purpose. Maybe they’re what pull people into the conversation in the first place.

If that’s the case, I’ll take it.

Because I’d rather see someone step into the world of personal finance— even through a loud, oversimplified doorway— than miss it entirely. (Look at me with my nuance.)