Budgeting Isn’t What You Think It Is

Key Takeaways

Budgeting done well isn’t about restricting your life.

Most people who feel guilty about not budgeting don’t actually know what budgeting entails.

Budgeting, like any skill, can be learned step by step.

The Observe–Track–Direct budgeting framework uses three simple behaviors to make budgeting more approachable.

For many people, the word budget has a bad reputation.

Do you like the word?

Maybe you imagine someone hunched over a calculator, stressing over a spreadsheet. Maybe you picture strict rules, constant restraint, and saying “no” to things you enjoy.

For a lot of people, budgeting sounds like a lifestyle of restriction, deprivation, and limitation.

If that’s what budgeting really were, it would make perfect sense to avoid it.

Many budgeting approaches jump straight to control.

Real humans are the ones implementing these methods. So budgeting strategies must take human nature into consideration!

How can a cumbersome, off-putting strategy work in real life?

My 3-phase budgeting method acknowledges reality—

People need to build

comfort

awareness

understanding

before they control their spending.

That’s why I designed my budgeting method to be

psychologically painless

beginner-friendly

easy to continue

empowering

customizable

financially powerful

Here’s the truth:

Budgeting done well isn’t about restricting your life.

It’s about directing your money toward the life you actually want.

Budgeting isn’t about telling yourself “no.”

It’s about deciding what matters most and telling your money where to go.

And when you learn how to do that, something remarkable happens.

Your money strengthens what matters most to you. That’s what I call growing money-strong.

Why So Many People Avoid Budgeting

Over the years, I’ve noticed something interesting while working with people who want to improve their finances.

Many of them say something like, “I know I should probably stick to a budget.”

But when we dig a little deeper, a surprising truth emerges. Most people who feel guilty about not budgeting don’t actually know what budgeting entails.

They have an idea of it, a stereotype of it, but they’ve never seen a practical, approachable way to do it.

You didn't learn to drive by telling yourself, "I just need to drive better."

You don't adopt healthy money habits by telling yourself, "I'm terrible. I know I just need to buckle down on my budget."

People assume budgeting is something disciplined people force themselves to do.

But budgeting isn’t a personality trait.

It’s a skill. And like any skill, it can be learned step by step.

My Own Fear of Budgeting

When I first started learning about personal finance at age 39, the idea of budgeting honestly terrified me.

Part of me expected it to be boring. But I was also scared. I was afraid to look closely at our money.

Questions ran through my mind:

Where exactly are all of our accounts?

How do I even log in to them?

Even if I find them, how do I know what to make of them?

Will it feel awkward talking with my husband about this?

How much does our household actually earn?

What if it’s not enough?

What if our expenses are all over the place?

If you’ve ever felt hesitant to look closely at your finances, you’re not alone.

A beach trip in November 2020, about 9 months before I started learning more than ever about personal finance.

Many people feel this way.

The turning point for me came when I realized something important:

Budgeting doesn’t have to happen all at once.

Budgeting Works Best in Phases

One reason budgeting feels overwhelming is that people think it requires doing everything at once.

They imagine immediately:

tracking every penny

creating strict categories

controlling every expense

That’s a lot to jump into if you’re just starting.

Budgeting becomes way more approachable when we break it into three simple behaviors that build on each other.

This is the framework I created for my clients, the Observe–Track–Direct budgeting framework.

Instead of trying to master everything at once, we grow these skills one at a time.

The three phases are:

1. Observe

First, simply learn to look at what your money is doing.

What money comes in?

What money goes out?

At this stage, we’re not trying to control anything. We’re just becoming familiar with our financial landscape.

Observation builds awareness.

And awareness is a step toward money strength.

This phase is important for a variety of people.

Many who tell themselves “I need to budget” aren’t all talk.

They take action— just not the best next action. They download a budgeting app. Maybe they even take the time to connect their accounts.

But then they don’t look at it again. A budgeting app might be humming away in the background. They might even be paying for a subscription. But they’re not budgeting– not because they didn’t want to take action, but because they didn’t take the right first step.

Many people sense that if they take a closer look at their money, they’ll have feelings and opinions— which could mean difficult conversations, hard choices, stress, and conflict.

If they’re fortunate enough not to have money problems demanding their attention, they can just preserve the status quo. They can stay afloat simply not checking on their money.

For the fearful and avoidant, the right next step is not full-fledged budgeting. It takes enough courage to start peeking at their accounts– with no pressure to calculate or fix anything.

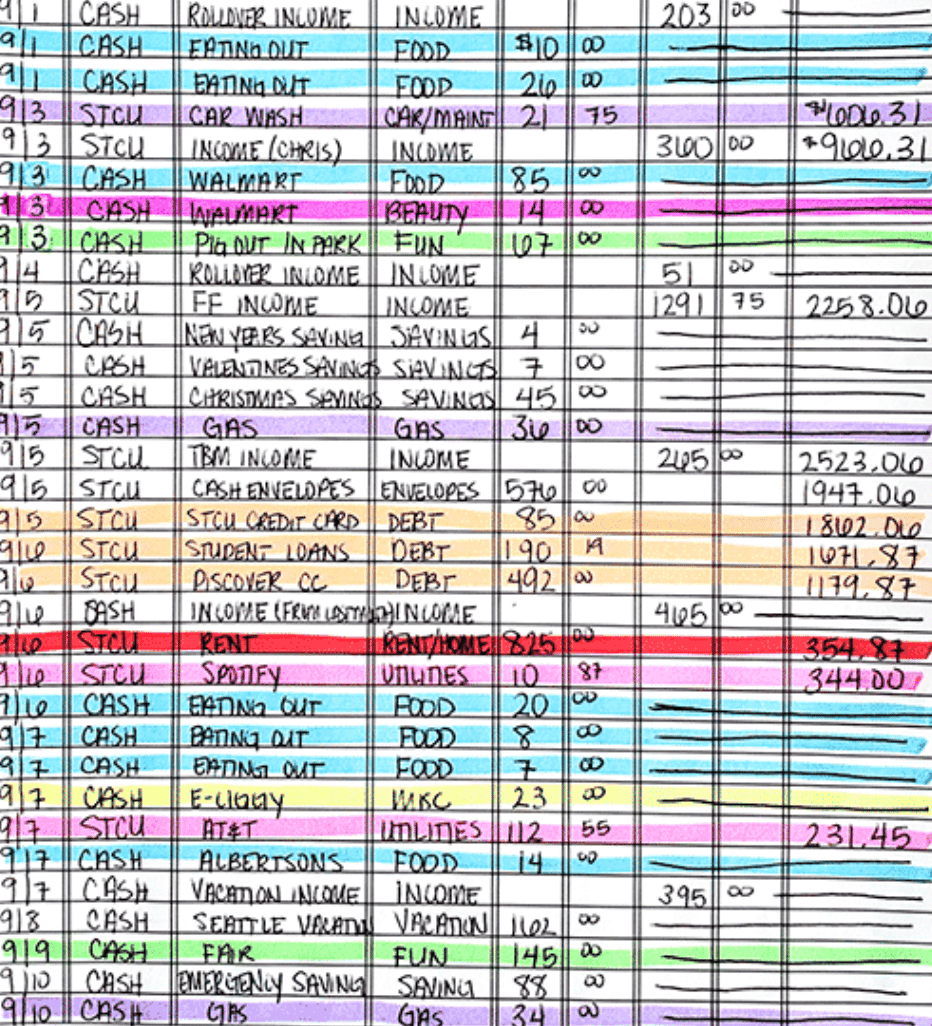

2. Track

Once observing feels comfortable, the next step is to record what you see.

Tracking means writing down your income and expenses over the course of a month.

In practice, this might happen on paper, using a budgeting app, in a note on your phone, or in a spreadsheet.

The "track" phase doesn’t entail restricting or controlling anything yet.

It simply turns observation into clear information.

When you track your money, you start to see patterns.

Instead of simply peering inside your accounts, you keep a record of running totals for the month. How much came in? How much went out?

You don’t have to work out the math; it might happen automatically in an app.

Patterns help you understand how your money supports what you care about (and leaks out into what you don’t).

After we begin analyzing our money's patterns, we develop opinions about how it can strengthen the goals and people we care about more than money.

Not only do you see and understand what your money does, but you also begin to form preferences about what you’d like it to do.

3. Direct

There are people who spend a lot of time managing a homemade spreadsheet. Despite what they call it, and despite the time they spend on it, sadly, they still aren’t budgeting.

They write down numbers, but they stop short of making sure the numbers make sense.

They fail to develop a plan.

Or if they write down a plan, they don’t make sure to implement it in real life.

They aren’t really budgeting because they’re missing the crucial final step: Direct.

Once you understand what your money is doing, you can develop preferences that allow you to draft a plan.

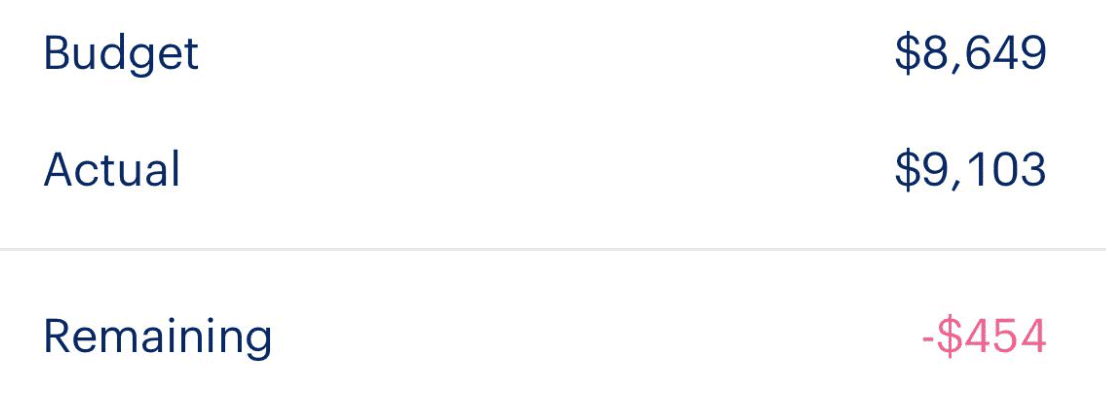

Before the month starts, you set rough target amounts for

Spending

Saving

Investing

Enjoyment

Finally, over the course of the month, you steer your money intentionally.

Directing your money means

planning where your money should go— in theory

making sure your money goes where it should— in reality

adjusting your planned amounts as needed, to match your actual amounts

When you direct your money, you tell your money where to go—and hold it accountable to going where you want it to.

To some extent, we all practice this third phase of budgeting. Whenever we make a spending decision, we are directing our money somewhere. But there is more to directing our money than simply making purchases.

And there is more to budgeting than simply sending our money somewhere; real budgeting means observation, tracking, and a plan, too.

When you set your expectations only after observing your accounts, tracking your money, and developing preferences, you set your plan up for success— because it’s based on your familiarity with reality.

Growing Money-Strong

These three phases work together to create full-fledged budgeting:

Observing your money builds comfort, familiarity, and awareness.

Track

Tracking your money builds understanding of how your money comes in and goes out.

Direct

Directing your money builds control. You take the driver's seat.

If this isn’t budgeting, then I don’t know what is.

And if “budgeting” isn’t this, then I don’t want to do it, either.

You don’t need to master these 3 behaviors overnight. Add the next only after you’re comfortable with the previous phase.

With patience and practice, budgeting stops feeling intimidating and starts feeling empowering.

Because once you learn how to guide your money with intention, something changes.

More and more, you see your money strengthen what matters most to you.

And that’s what growing money-strong is all about!