The Second Behavior of Budgeting: Track Your Money

Key Takeaways

Tracking your money simply means recording your income and expenses over the course of a month.

Tracking doesn’t require complicated tools.

Some people who say they keep a budget don't actually do what I consider real budgeting.

Sometimes they think they're budgeting because they keep a list or spreadsheet.

In my view, keeping a record of certain key numbers can be powerful, but only if joined with the other two essential habits of budgeting.

In my Observe–Track–Direct budgeting framework, budgeting stems from three simple behaviors:

Observe – look at what your money is doing

Track – record what you see

Direct – intentionally plan where your money will go

Once observing becomes a regular habit, you’re ready for the next step: tracking your money.

What It Means to Track Your Money

Tracking your money simply means recording your income and expenses over the course of a month.

When you observe, you receive information by looking at your accounts.

When you track, you take that information and write it down somewhere.

This step transforms vague impressions into clear data.

Instead of guessing how much money is coming in and going out, you can actually see the totals.

And that clarity is powerful.

Tracking Gone Wrong

Some people’s money stress inspires them to “track” with homegrown spreadsheets or unwieldy paper notes.

Yet their documentation produces confusion and overwhelm rather than clarity and control.

When a tracking attempt goes awry, it’s often because the record is incomplete, hard to interpret, and disconnected from a larger plan.

The author of such a document might feel unclear on certain personal finance concepts.

The document becomes an expression of confusion rather than a solution to it.

Without the other two phases of budgeting—observe and direct—the attempt to track can cause more harm than good.

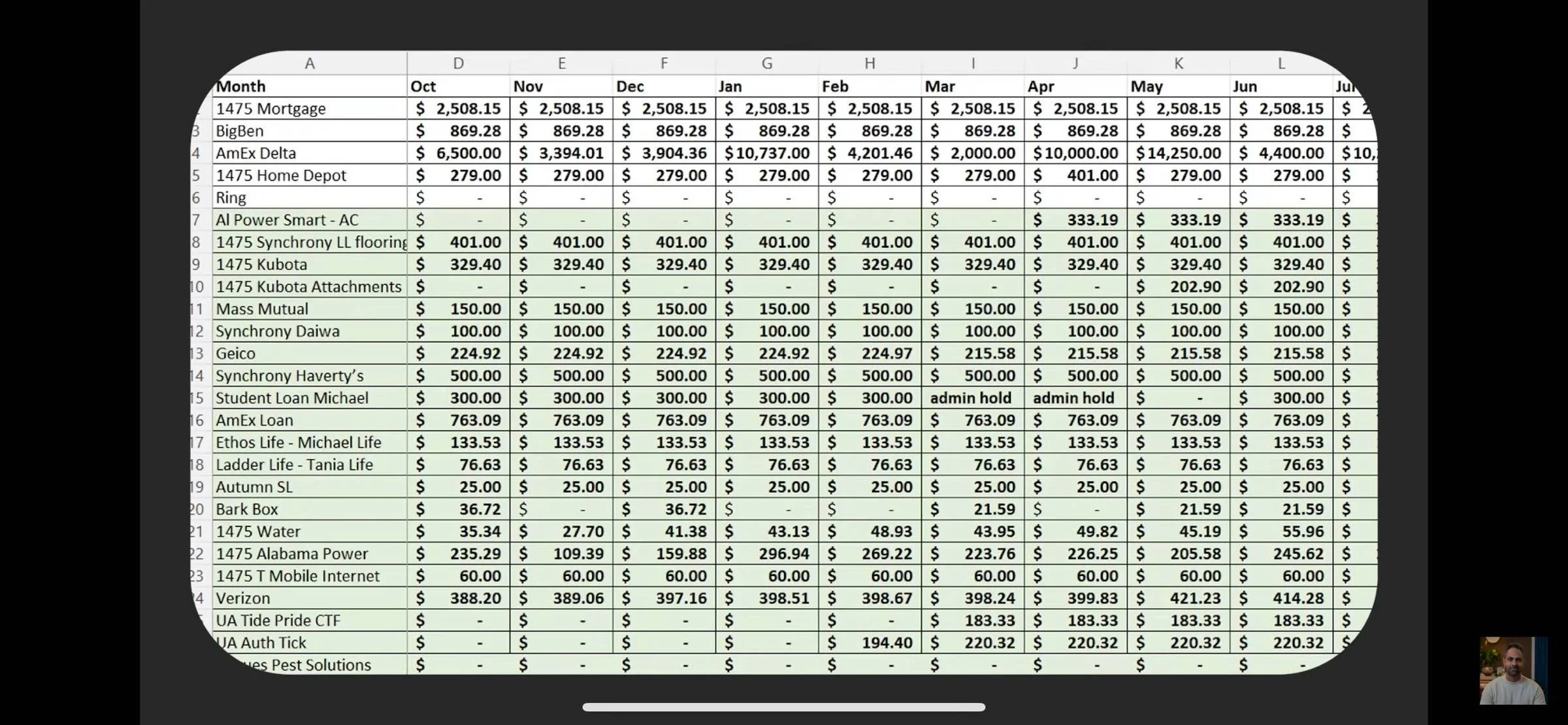

Ramit Sethi’s “Money for Couples” guests Tania and Mike experienced this problem.

They struggled with debt and overspending all 20 years of their marriage, even while Tania maintained a spreadsheet.

Tania's spreadsheet looks overwhelming.

Her spreadsheet was incomplete, focused narrowly on loan minimum repayments and due dates.

This may have resulted from the all-too-common mistake of focusing too much on monthly payments, to the neglect of other important numbers. I teach ways to strengthen your net worth mindset, to counteract this common imbalance.

This type of behavior looks like tracking, but it’s not what I envision for phase two of my Observe-Track-Direct framework.

This type of “tracking” creates a sensation of budgeting—in the absence of true budgeting behaviors and results.

Tracking Doesn’t Mean Restricting

One reason people hesitate to track their money is that they assume it means immediately controlling every expense.

But tracking doesn’t require that.

At this stage, you’re still not trying to manipulate or restrict your spending.

You’re simply building a clear picture of what is already happening.

Think of tracking as collecting information.

It’s a way of answering questions like:

How much money comes in each month?

How much goes out?

Where does it tend to go?

Without this information, directing your money later becomes much harder.

How to Track Your Money

The good news is that tracking doesn’t require complicated tools.

You can use whatever method works best for you.

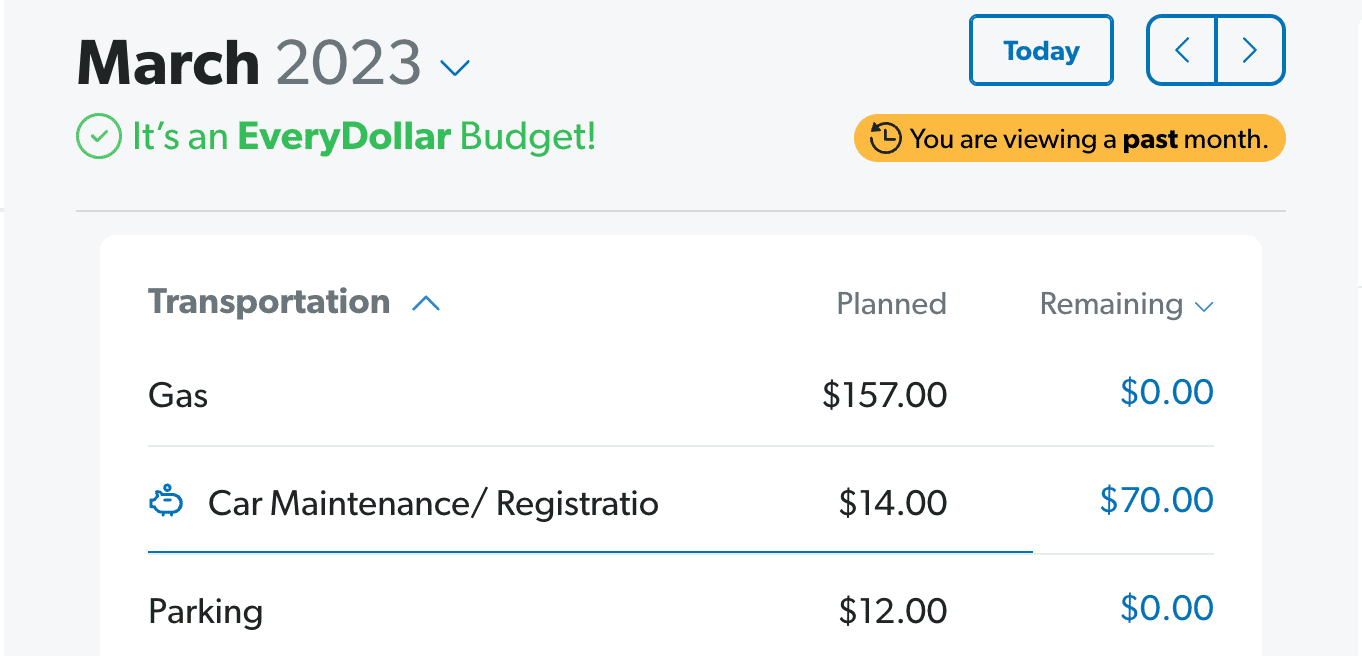

The free version of Every Dollar allows you to enter numbers manually. I like to round to the nearest dollar to make the numbers look cleaner and simpler.

Some people prefer:

pen and paper

a note on their phone

a spreadsheet

a budgeting app

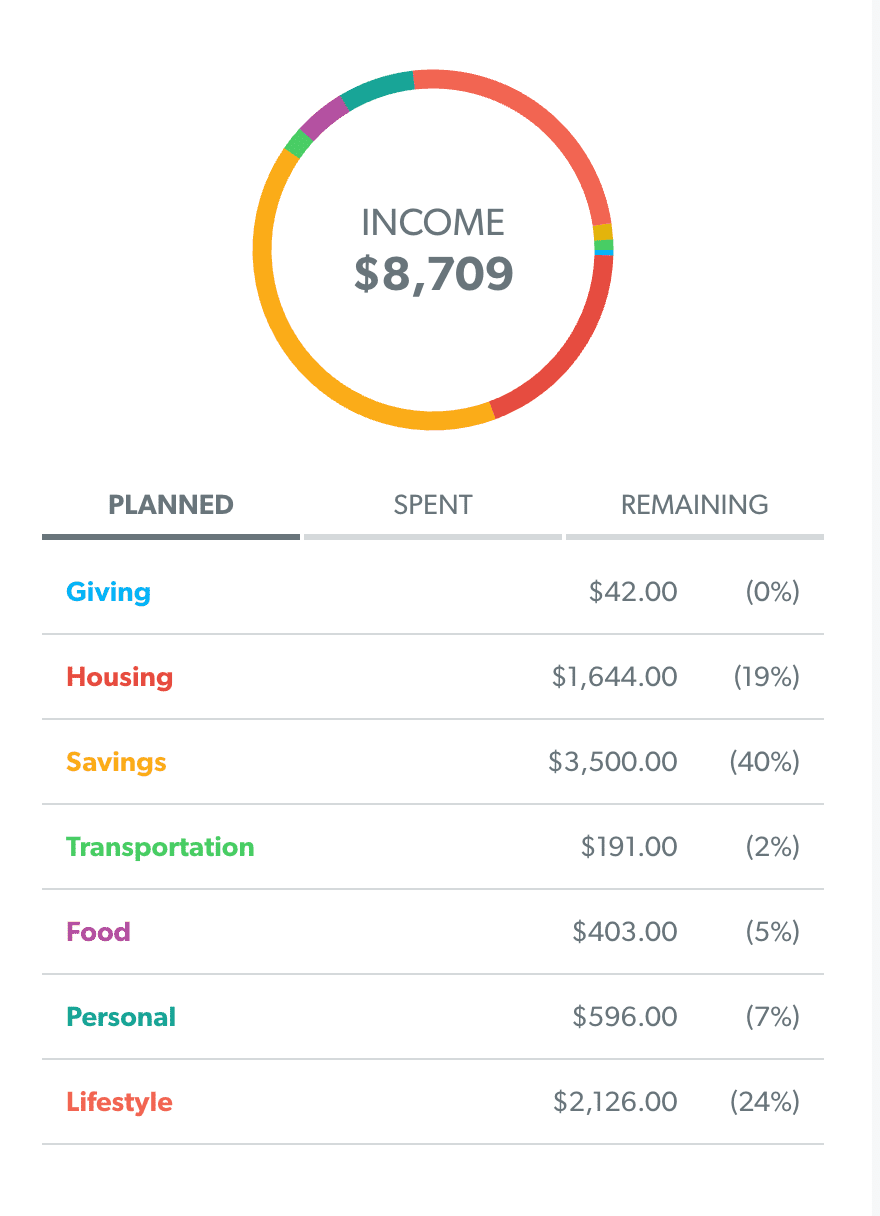

Some checking accounts and credit cards provide tracking information with pie charts and totals added up for you.

PNC accounts break down spending for you.

The specific tool doesn’t matter. Choose something simple that feels most appealing to you.

Start With Just Two Categories

When people begin tracking their money, they sometimes feel tempted to create dozens of detailed categories.

But that isn’t necessary at the beginning.

You can start with just two:

Income

Expenses

Throughout the month, record the money that comes in and the money that goes out.

Calculate your running totals as the month progresses.

By the end of the month, you’ll see exactly how much money came in and how much went out.

That alone provides valuable insight.

Adding a Few Helpful Categories

Once you’re comfortable tracking your income and expenses using two categories, you may want to add a few simple categories for more insight.

I recommend four broad categories:

Baseline Costs – essential living expenses

Saving – money set aside for future needs

Investing – money growing for long-term goals

Enjoyment – money spent on things that make life enjoyable

Generosity might fall under baseline costs or enjoyment, depending on the priority and regularity of your charitable giving.

These categories help you see how your money supports different areas of your life.

You can also calculate the percentage of your income going toward each category.

This can reveal helpful patterns and spark thoughtful conversations about your priorities.

Why Tracking Matters

Tracking does something important.

It turns observation into understanding.

Instead of relying on assumptions, you begin working with real numbers.

Sometimes those numbers confirm what you expected.

Other times they reveal surprises.

Either way, they give you the information you need to move forward.

And once you understand what your money is doing, you’re ready for the next step: directing it with intention.

Building up to Budgeting

Some people track their money and call it “budgeting.”

In my view, merely tracking is insufficient.

But it’s an essential step.

Observation builds awareness.

Tracking builds understanding.

And understanding prepares you for the final phase of the Observe–Track–Direct budgeting framework—learning to guide your money toward the things that matter most.