The Financial Advisor Scheme That Shouldn’t Be Legal (But Is)

Key Takeaways

Multi-level marketing companies don’t just sell knives and cleaning rags, but personal finance products.

The participant thinks they’re a salesperson when they’re really a consumer, driving economic success for the organization rather than for themselves.

Anyone can legally market themselves as a financial advisor, wealth manager, investment advisor, or financial planner.

When someone is selling a product for a commission, their incentive might be at odds with your needs— an inherent conflict of interest.

Research suggests that a significant majority of participants in MLMs lose money or earn very little—sometimes less than minimum wage when time is factored in.

I was recently on a group call for entrepreneurs learning about marketing.

During the call, another participant messaged me privately. She said we did similar work and asked if I’d schedule a call with her.

She mentioned she was pivoting into wealth management. I’m a financial coach, so that sounded like a natural connection.

We scheduled a call.

During our conversation, I learned that she was involved in a multi-level marketing (MLM) company selling life insurance products. She had hit rock bottom financially 6 months earlier, when a friend called, offering a wealth-building opportunity.

She didn’t explicitly pitch me on anything. She said she wanted to tell me more about the life insurance products and meet again the following week.

She mentioned she’s attending as many networking events as possible to find clients.

After the call, I found myself wondering:

How many other people from that group received the same message?

Did You Know Financial MLMs Are a Thing?

If this is new to you, you’re not alone.

I first encountered this world about three years ago when I attended what I thought was a job interview.

An acquaintance connected me with his friend. He called me because his company was looking to hire financial coaches to guide clients and help families.

We shared enthusiasm about personal finance education. (Oops, I forgot to ask the name of the company!)

When I entered the office for the “interview,” I walked into a recruitment pep rally.

The recruiters brought me into a dark room with a few dozen people, upbeat pop music blasting loudly, everyone standing, cheering, and energized.

The company was Primerica.

That’s when I learned that MLMs don’t just sell knives and cleaning rags, but personal finance products.

A couple salespeople shared tearful testimonies about how selling for Primerica transformed their lives. Just a few months ago, they had no aim and no job. Now they were making more money than they ever imagined, all while helping others grow their wealth.

A recruiter spoke with me individually. He said they were all financial coaches, exactly like me, just trying to coach people in personal finance.

I told him my own financial coaching business was on the back burner while I took a full-time job teaching at a public elementary school. He said it was no problem if I didn’t have time to sell financial products— I could simply recruit a few friends and family members to sell for Primerica, then collect a cut from each sale they made. I would get effortless income!

How Financial MLMs Work

At a high level, financial MLMs operate like other MLMs.

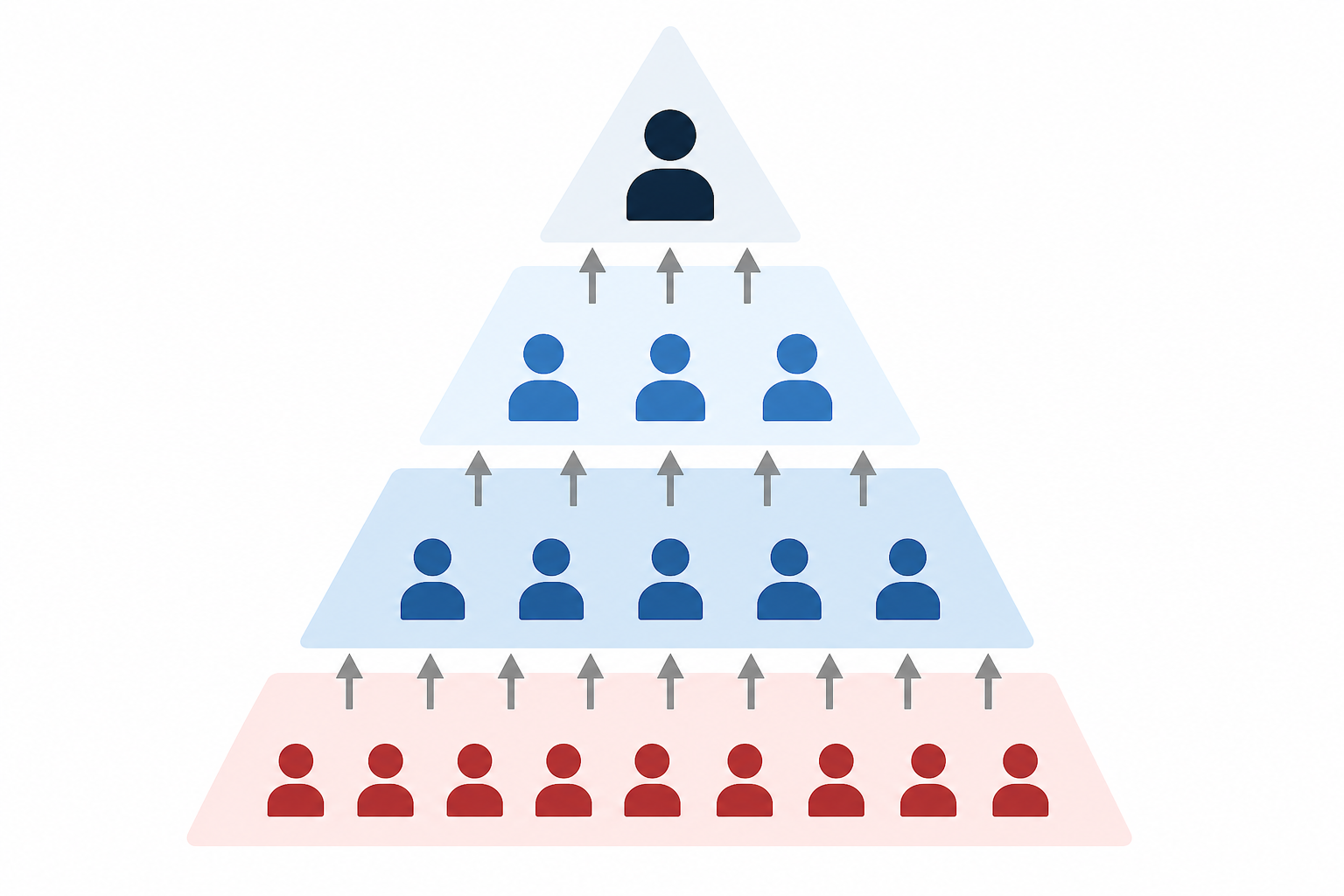

Recruitment-driven income

Participants earn money not just from selling products, but from recruiting others into the business.

This creates a “downline,” where income is tied to the performance of people you bring in.

Licensing and products

Participants are encouraged to take tests to get licensed to sell financial products. Many people say the tests are surprisingly easy.

Their products can include:

life insurance policies

annuities

investment-related products

These products are often complex, and the people selling them may be brand new to personal finance.

A Primerica advisor’s recruitment video explains how a large portion of a client’s insurance premium goes toward the advisor’s compensation.

High-pressure networking

Participants are often told to:

attend networking events

reach out to friends and family

book as many conversations as possible

The goal is to find both clients and recruits.

This can blur the line between genuine connection and business development.

The Problem With the Business Model

One of the most confusing aspects of MLMs is how they position participants.

Recruits are often made to feel like:

entrepreneurs

business owners

financial professionals

But in reality, they are usually:

incentivized to sell their high-commission products, regardless of a client’s needs

incentivized to tout the financial benefits of selling, to create their downline

not earning much

This creates a strange dynamic where the participant thinks they’re a salesperson when they’re really a consumer, driving economic success for the organization rather than for themselves.

On Financial Advisors

To understand why this matters, it helps to distinguish between different types of financial professionals.

What is a financial advisor?

Technically, a financial advisor is anyone who wants to call themselves a financial advisor. This may seem strange— and it is.

There is no regulation of the term “financial advisor.”

In the personal finance world, we commonly reserve the term for professionals licensed to sell investment advice.

This point deserves reiteration:

Anyone can legally market themselves as a financial advisor, wealth manager, investment advisor, or financial planner.

The title “financial advisor” itself denotes nothing in particular.

The U.S. Securities and Exchange Commission (SEC) issued a helpful bulletin, stating:

“A financial professional may use various titles whether or not he or she is registered or licensed with a regulatory authority.”

“Some titles are granted by private organizations, such as a trade group. While some private groups that grant titles may provide a method for you to complain about one of their members and can discipline a member for misconduct, there are other groups that do not take complaints or discipline their members.

Still other titles may be simply purchased, or even made up by financial professionals hoping to imply that they have certain expertise or qualifications; such titles are generally marketing tools and are not granted by a regulator.”

“Like the SEC and state securities regulators (NASAA), FINrA does not grant, approve or endorse any professional designation.”

Commission-based advisors

These advisors earn money by selling financial products.

If they sell you a policy or investment, they receive a commission.

Fee-based advisors

These advisors may charge fees and earn commissions.

I’ve often heard the term “fee-based” confused with “fee-only.”

Fee-only advisors

These advisors are paid only by their clients.

They do not earn commissions from selling products.

They might collect a fee in the form of a percentage of “assets under management” (AUM), meaning they regularly pull out a percentage of the investment portfolio they manage. If the portfolio balance grows exponentially, their fee grows exponentially.

Alternatively, a fee-only advisor might collect a payment amount that remains stable, regardless of the portfolio balance. This is called a “flat fee.”

I’ve often heard people use “fee-only” when they mean “advice-only.”

Advice-only advisors

These advisors provide guidance but do not manage investments or sell products. Clients and I have enjoyed the advice-only firm, Nectarine.

They are paid strictly for their advice.

What is a fiduciary?

A fiduciary is someone legally required to act in your best interest.

Not all financial advisors are fiduciaries.

Some operate under a lower standard, meaning they only need to recommend products that are “suitable,” not necessarily the best option for you.

And some advisors are just people who call themselves advisors.

These distinctions matter.

When someone is selling a product for a commission, their incentive might be at odds with your needs— an inherent conflict of interest.

The Problem With the Product

Let’s talk about a commonly promoted product in financial MLMs:

Indexed Universal Life (IUL) insurance policies

These are often marketed as:

a way to build wealth

an alternative to traditional investing

a safe growth strategy

But in reality, they are:

complex

expensive

insurance products with an investment-related component (not investments)

I recently had a client ask me if they should purchase one of these policies. Friends were recommending it. We were both grateful to discuss it together before my client tied money up in an expensive IUL.

These products are not the right starting point for the average adult trying to grow strong with money.

The loudest voices in favor of IULs are the people and companies selling them.

Critics include:

Ramsey Solutions, “Indexed Universal Life Insurance (IUL), Explained”

Personal Finance Club, “Is IUL a scam? Yes.”

Ramit Sethi, “How Much Life Insurance Do I Need?”

What Experts Say

There’s growing awareness around MLMs in general.

Advocates like Roberta Blevins and personal finance voices like Jeremy Schneider have spoken about the risks and realities of this business model.

Research suggests that a significant majority of participants in MLMs lose money or earn very little—sometimes less than minimum wage when time is factored in.

And when it comes to personal finance MLMs, the stakes can be even higher—because now we’re talking about people’s financial futures.

When It Feels Like Something Is Off

If you’ve ever been approached about an “opportunity” like this, you might have felt a mix of:

curiosity

pressure

confusion

That’s intentional.

These systems are often designed to feel:

exciting

empowering

urgent

MLM recruitment tactics appeal to those looking for work flexibility.

In How to Get Rich on Netflix, Ramit Sethi speaks with Christian and Millie. Millie is involved in an MLM. Sethi gently but clearly points out how these systems can blur reality, making it difficult to distinguish between hope and actual financial outcomes. In a later follow-up video, Millie shares that she hadn’t given up the MLM.

Risks and Red Flags

If you’re evaluating a financial opportunity like this, here are a few things to watch for:

A strong emphasis on recruiting others

Pressure to attend frequent meetings or events

Requests to pay upfront fees for training or licensing

Complex products that are hard to explain simply

Vague or unclear income expectations

You can also ask for an income disclosure statement to see how much participants actually earn.

A More Grounded Approach to Becoming Money-Strong

One of the reasons I care about this topic is because I’ve seen how easily people can be led away from simple, effective financial habits.

Becoming money-strong doesn’t require:

complicated products

aggressive sales tactics

or joining a business opportunity

It involves developing a well-rounded set of financial habits and perspectives over time.

In my work with clients, I define money strength as growth in several key areas:

tracking your net worth

updating your money mindset

saving intentionally

investing thoughtfully

understanding your values (what matters more to you than money)

and remaining a lifelong student of personal finance

These are the skills that build lasting confidence with money.

They’re reliable, realistic, practical, and powerful.

How to Talk to a Loved One Involved in an MLM

If someone you care about is involved in a financial MLM, this can be a sensitive situation.

You may feel concerned. You may want to help. But you also don’t want to damage the relationship.

It’s a difficult balance.

Experts like Steven Hassan, who has studied high-control groups, emphasize the importance of approaching these conversations with empathy rather than confrontation.

A few helpful principles:

Lead with curiosity, not criticism

Instead of telling them they’re wrong, ask questions:

“What do you like about it?”

“How does the income structure work?”

“What has your experience been so far?”

This keeps the conversation open.

Avoid direct attacks on the business

If you immediately criticize the company, your loved one may feel defensive and shut down.

Remember, they may have invested:

time

money

identity

into this.

Gently encourage independent thinking

You might ask:

“Have you seen the company’s income disclosure statement?”

“How many people actually earn what you’re attempting to earn?”

Invite reflection without applying pressure.

Stay connected

The most important thing is preserving the relationship.

If they ever begin to question their involvement, they’ll be more likely to come to you if they feel safe and respected.

The Bottom Line

Financial MLMs are legal.

But legality doesn’t always mean something is helpful, ethical, or in your best interest.

If someone approaches you with a financial product or opportunity, it’s okay to:

ask questions

take your time

seek a second opinion

Your financial life is too important to hand over to a system you don’t fully understand.

You deserve clarity.

You deserve confidence.

And you deserve a financial approach that truly supports what matters most to you.